For many small business owners, that is not a hypothetical scenario, it’s Tuesday morning.

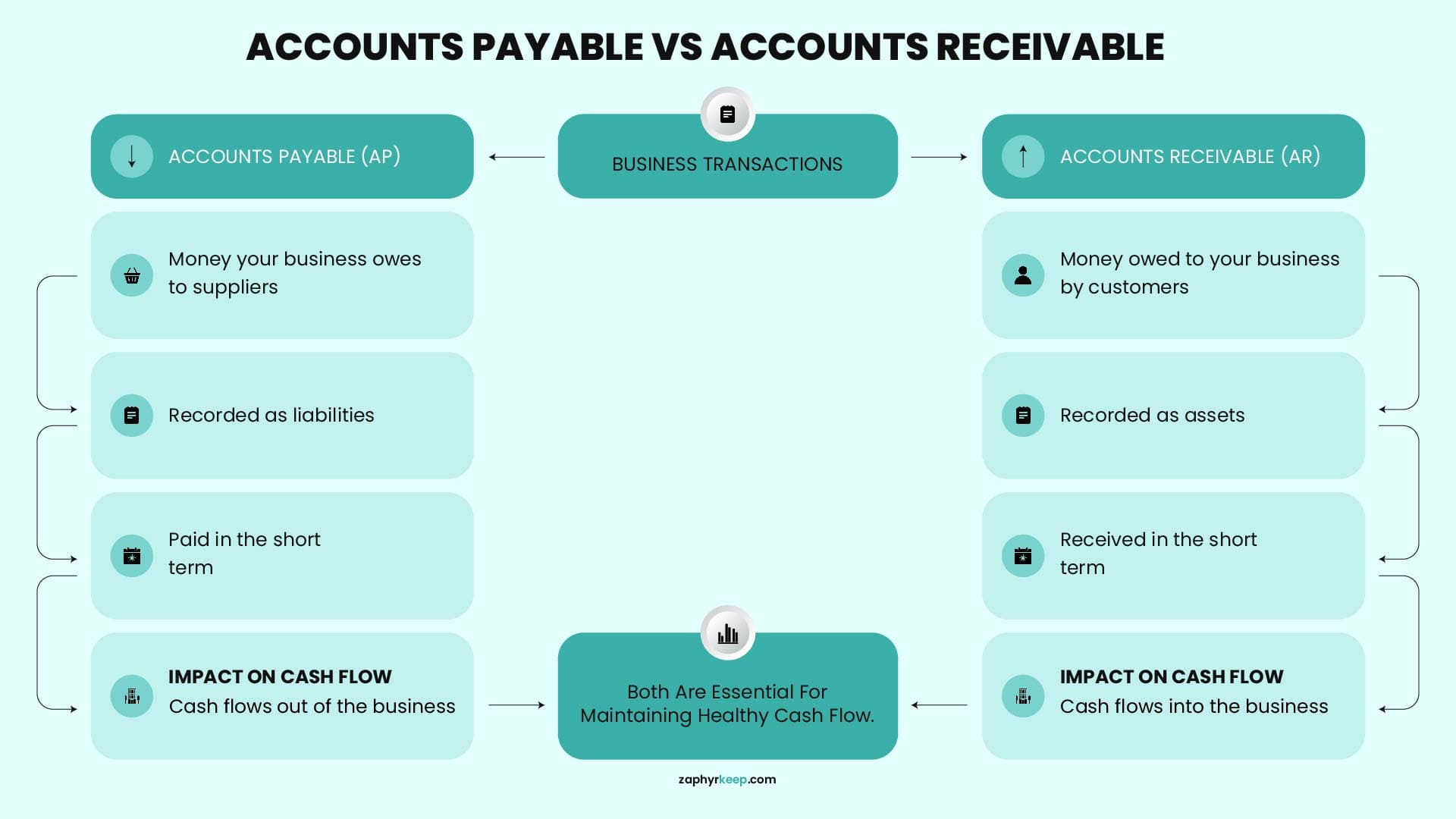

Accounts payable (AP) and accounts receivable (AR) are two of the most basic ideas in business finance. They sit on opposite sides of every credit transaction, but business owners still mix them up more often than you’d think. One is money going out. The other is money coming in. Simple at first, but not always in practice. Get them wrong in your books, and your balance sheet starts telling the wrong story. Your tax filings can become inaccurate, your cash flow forecasts lose trust, and your financial decisions sit on a shaky foundation.

This guide walks you through the confusion with plain-language definitions, real examples, journal entry walkthroughs, and the latest data on how AP and AR mismanagement costs businesses in 2025, helping you prepare for what’s ahead. Give it the next 8 minutes, and by the end, the difference between AP and AR will feel clear, practical, and easy to apply.

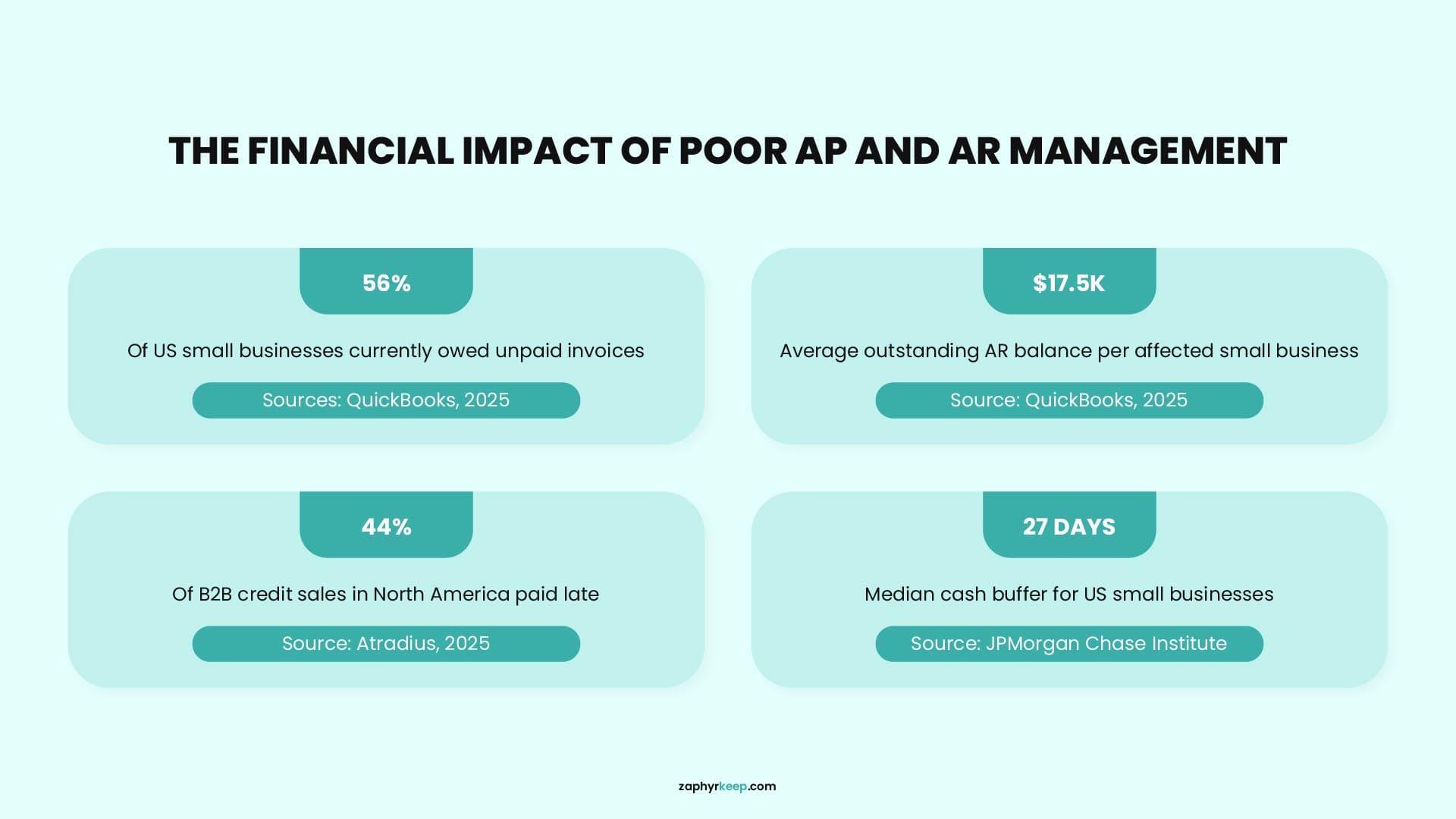

Behind every unpaid invoice, delayed supplier payment, and unexpected cash flow crunch is a process that isn’t working as it should. The data shows that businesses continue to lose time, money, and financial visibility because of avoidable AP and AR mistakes.

Accounts Payable vs Accounts Receivable: Core Definitions

At the most fundamental level, the difference between accounts receivable and accounts payable comes down to direction. Is money coming into your business, or is it leaving your business? Every credit transaction can be traced back to one of these two movements.

Accounts Payable (AP) – Money your business owes

AP is a liability on your balance sheet. It records all the short-term debts your company owes to vendors, suppliers, and service providers for goods or services received on credit but not yet paid for.

Accounts Receivable (AR) – Money owed to your business

AR is an asset on your balance sheet. It records all the money customers and clients owe you for goods or services you have already delivered, but for which you have not yet received payment.

Think of it this way: if you are a freelance designer and you send a client an invoice for a completed website, that unpaid invoice lives in your accounts receivable until the client pays. Meanwhile, the subscription fee you owe your design software provider sits in your accounts payable until you pay it.

Understanding the direction of money flow is the first step. The next question is just as important: where do accounts receivable and accounts payable actually sit on your balance sheet, and why does that classification matter?

What type of account is accounts receivable?

Accounts receivable is classified as a current asset on the balance sheet. It is current because the expectation is that the customer will pay within a year, typically within 30 to 90 days depending on the agreed payment terms. Since it represents future cash the business expects to receive, it holds real financial value and increases the company’s total assets.

What type of account is accounts payable?

Accounts payable is a current liability. It reflects short-term obligations the business must settle, typically within the vendor’s payment terms. High AP relative to available cash can signal liquidity pressure. However, strategically managing payment timing within agreed terms is a legitimate cash flow tool used by businesses of every size.

Accounts Payable vs Accounts Receivable: Key Differences

The table below captures the full picture of what is accounts payable vs accounts receivable across every major dimension.

|

Factor

|

Accounts Payable (AP)

|

Accounts Receivable (AR)

|

|---|---|---|

|

Definition

|

Money your business owes to others

|

Money others owe to your business

|

|

Balance sheet classification

|

Current liability

|

Current asset

|

|

Cash flow direction

|

Outflow (you pay)

|

Inflow (you collect)

|

|

Created when

|

You receive goods/services on credit

|

You deliver goods/services on credit

|

|

Closed when

|

You pay the vendor/supplier

|

Customer pays you

|

|

Role in journal entry

|

Credited when created; debited when paid

|

Debited when created; credited when paid

|

|

Risk if mismanaged

|

Late fees, damaged vendor relationships

|

Bad debt, cash flow shortfalls

|

|

Linked department

|

Finance / procurement

|

Sales / finance / collections

|

|

Common metrics

|

Days Payable Outstanding (DPO)

|

Days Sales Outstanding (DSO)

|

Accounts Payable vs Accounts Receivable Examples

Theory is helpful, but the distinction becomes much easier to understand when you see it in action. Here are a few real-world examples showing how accounts payable and accounts receivable work together in everyday business operations.

Example 1: A Marketing Agency

Elevate Creative, a digital marketing agency, has just wrapped up a brand campaign for a retail client. It sends an invoice for $12,000 with net-30 payment terms. Until that payment arrives, the amount is recorded as accounts receivable because the agency has earned the revenue but has not yet collected the cash.

At the same time, Elevate owes $2,400 to a freelance copywriter who contributed to the project. Since that payment is still outstanding, it appears in accounts payable.

One transaction brings money into the business, while the other represents money going out. That’s a clear example of how AP and AR often exist side by side within the same project.

Example 2: A Wholesale Distributor

A food distributor receives a shipment of olive oil worth $45,000 from a European supplier on net-60 payment terms. Because the invoice has not yet been paid, the amount is recorded as accounts payable.

The distributor then sells that inventory to three restaurant chains on net-30 terms, generating $60,000 in accounts receivable. In this situation, the business expects to collect cash from customers before its payment to the supplier comes due.

When incoming payments arrive faster than outgoing obligations, businesses gain flexibility and maintain healthier cash flow.

Example 3: A Construction Company

A general contractor completes a project and invoices a property developer for $280,000. Until payment is received, that amount sits in accounts receivable.

At the same time, the contractor still owes an electrical subcontractor $40,000 for work completed earlier in the project. That outstanding balance is recorded as accounts payable.

Problems arise when those timelines don’t align. If the developer delays payment for 60 days but the subcontractor expects payment within 30, the contractor may face a temporary cash shortage despite having significant revenue on paper. Situations like this are common in construction, where payment cycles are often longer than in many other industries.

Note: Cash sales never create accounts receivable. If a customer pays immediately at the point of sale, the transaction is recorded as cash revenue. Accounts receivable only exists when goods or services are delivered today and payment is expected at a later date.

Journal Entries and the Balance Sheet

By now, the difference between accounts payable and accounts receivable is probably clear. The next step is understanding how they are actually recorded in your books.

This is where journal entries come in. Every invoice you send, bill you receive, payment you collect, and expense you settle leaves an accounting trail. Journal entries are simply the records that capture those transactions and ensure your financial statements reflect what’s really happening inside the business. Get the entries right, and your books stay accurate. Get them wrong, and small mistakes can quickly spread across your balance sheet, cash flow reports, and financial statements.

Accounts Receivable Journal Entry

Let’s say your business completes a service and sends a customer an invoice for $5,000. Even though the cash hasn’t arrived yet, you’ve earned the revenue, so the transaction needs to be recorded.

Journal Entry: Recording a Sale on Credit

|

Account

|

Debit

|

Credit

|

|---|---|---|

|

Accounts Receivable

|

$5,000

|

|

|

Revenue

|

|

$5,000

|

When the customer pays the invoice, the receivable is cleared and cash increases.

Journal Entry: Recording Customer Payment

|

Account

|

Debit

|

Credit

|

|---|---|---|

|

Cash

|

$5,000

|

|

|

Accounts Receivable

|

|

$5,000

|

Accounts Payable Journal Entry

Now consider the opposite side of the transaction. Your business receives supplies worth $3,200 from a vendor, but payment isn’t due immediately. Because you’ve received the goods but haven’t paid for them yet, the amount is recorded as accounts payable.

Journal Entry: Recording a Purchase on Credit

|

Account

|

Debit

|

Credit

|

|---|---|---|

|

Supplies / Inventory

|

$3,200

|

|

|

Accounts Payable

|

|

$3,200

|

Once the vendor is paid, the liability is removed from your books and cash decreases.

Journal Entry: Recording Vendor Payment

|

Account

|

Debit

|

Credit

|

|---|---|---|

|

Accounts Payable

|

$3,200

|

|

|

Cash

|

|

$3,200

|

On the balance sheet, accounts receivable increases total assets because it represents money the business expects to collect. Accounts payable increases total liabilities because it represents money the business owes to others.

For example, a company with $100,000 in accounts receivable and $30,000 in accounts payable may appear to be in a strong position. However, that only holds true if those receivables are actually collectible. If customers fail to pay, the outstanding balances may need to be written off as bad debt, reducing both assets and profitability. That’s why managing collections is just as important as generating sales.

Did you know? Accurate AP and AR records make bank reconciliation much easier. If your books show a payment that doesn’t appear in your bank account, reconciliation is often where the discrepancy is discovered. Learn how bank reconciliation works and why it matters.

The AP and AR Processes Explained

Knowing the difference between accounts payable and accounts receivable is one thing. Managing both correctly is where the real work begins. AP controls how money leaves the business. AR controls how money comes back in. When either process is loose, cash flow becomes harder to predict.

The Accounts Payable Process

Accounts payable is not just about receiving a bill and paying it. In a well-run business, AP follows a controlled process that helps prevent duplicate payments, invoice errors, vendor disputes, and fraud.

Typical AP workflow:

|

Step

|

Stage

|

What Happens

|

|---|---|---|

|

1

|

Purchase Order

|

The buyer creates and approves a purchase order.

|

|

2

|

Goods or Service Receipt

|

The business confirms that goods or services were received.

|

|

3

|

Invoice Receipt

|

The vendor sends an invoice for payment.

|

|

4

|

Three-Way Match

|

The PO, receipt, and invoice are checked against each other.

|

|

5

|

Payment

|

Payment is issued according to the agreed terms.

|

The most important checkpoint is the three-way match. This step compares what was ordered, what was received, and what was invoiced. If the numbers do not match, the payment should be reviewed before money leaves the business.

Skipping this step can lead to overpayments, duplicate payments, or even invoice fraud.

The Accounts Receivable Process

Accounts receivable starts when a business agrees to let a customer pay later. That sounds simple, but AR can quickly become a cash flow problem if invoices are delayed, payment terms are unclear, or follow-ups are inconsistent.

Typical AR workflow:

|

Step

|

Stage

|

What Happens

|

|---|---|---|

|

1

|

Credit Check

|

The business reviews customer risk before offering credit.

|

|

2

|

Deliver Goods or Services

|

Work is completed or products are delivered.

|

|

3

|

Issue Invoice

|

The customer receives a clear invoice with payment terms.

|

|

4

|

Track and Follow Up

|

The invoice is monitored through aging reports and reminders.

|

|

5

|

Collect and Post Payment

|

Payment is received, recorded, and reconciled.

|

The step many small businesses skip is the credit check. It is tempting to accept every new customer, especially when revenue feels urgent. But extending credit without checking risk is one reason receivables age, collections slow down, and earned revenue never turns into cash.

If tracking AP, AR, invoices, payments, and reconciliations is becoming too time-consuming, outsourced bookkeeping can help keep these processes organized without adding more manual work to your team.

How AP and AR Affect Cash Flow

The relationship between AP, AR, and cash flow is direct. A business can be profitable on paper yet insolvent in practice if it collects payments slowly while obligations pile up. This is the working capital gap, and it destroys businesses that do not manage it deliberately.

The working capital equation

Working capital is calculated as: Current Assets minus Current Liabilities. AR is a current asset. AP is a current liability. So a business with $200,000 in AR and $80,000 in AP has $120,000 in working capital, assuming those receivables are collectible. If $60,000 of the AR is 90 days overdue and likely uncollectible, real working capital is just $60,000. That discrepancy matters enormously for cash planning.

Strategic AP management

Sophisticated businesses do not just pay AP invoices as they arrive. They pay strategically. This means capturing early payment discounts when the math works out (a 2/10 net 30 discount is effectively an annualized return of around 36%), and otherwise holding payment until the due date to preserve cash. However, this requires accurate AP records. Paying late by accident, rather than by choice, damages vendor relationships and can result in supply disruptions.

Key Metrics to Track for AP and AR

Fnancial ratios, because AP and AR only become useful when you can see whether cash is moving faster, slower, or getting stuck.

Days Sales Outstanding (DSO)

DSO measures how long on average it takes to collect payment after a sale.

Formula: (AR / Total Credit Sales) x Number of Days.

A rising DSO signals slowing collections. A falling DSO means customers are paying faster. Construction and manufacturing industries consistently show the highest DSO, meaning businesses in those sectors need larger cash buffers to sustain operations between invoicing and collection.

Days Payable Outstanding (DPO)

DPO measures how long a company takes to pay its suppliers.

Formula: (AP / Cost of Goods Sold) x Number of Days.

A higher DPO means you hold cash longer before paying, which is positive for liquidity as long as you stay within agreed terms and do not damage supplier relationships.

Accounts Receivable Turnover Ratio

This ratio shows how many times per year a business collects its average AR balance.

Formula: Net Credit Sales / Average AR.

A higher number is better. It signals efficient collections and healthy customer payment behavior.

Pulling It Together: AP, AR, and Your Business Health

Understanding accounts receivable vs payable is not just about knowing where each transaction goes. It is about knowing what your business is owed, what it needs to pay, and how much cash you can actually count on.

When receivables are not followed up, money stays stuck in unpaid invoices. When payables are not tracked, bills get missed, vendors get frustrated, and late fees become avoidable expenses. Over time, these small gaps can make your finances harder to manage than they need to be.

That is why AP and AR should not be treated as simple admin tasks. They are part of how your business protects cash flow, plans ahead, and makes better decisions.

Stop Letting AP and AR Manage You

ZaphyrKeep helps small businesses keep their books clean, organized, and up to date, so invoices, payments, and reconciliations do not slip through the cracks. You get a clearer view of what is coming in, what is going out, and where your cash flow stands, without having to chase every detail yourself.

Explore ZaphyrKeep’s bookkeeping services and keep your AP, AR, and cash flow under control.

Key Takeaways

- Bank reconciliation matches your internal records against your bank statement and explains every single difference between them.

- Differences almost always come from timing issues (checks that haven’t cleared, deposits in transit), missed entries (bank fees, interest), or human errors.

- A completed reconciliation gives you your true cash position so you stop guessing which balance is right.

- Regular reconciliations catch small mistakes before they turn into audit problems, fraud losses, or bad business decisions.

|

Factor

|

In-House Bookkeeping

|

Outsourced Bookkeeping

|

|---|---|---|

|

Cost

|

Salaries, benefits, training, and software costs add up

|

Pay for services as needed, often cheaper in the long run

|

|

Control

|

Direct oversight, instant access to financial data

|

Less control, but reports and updates are scheduled

|

|

Scalability

|

Hiring new staff is expensive and time-consuming

|

Scale services up or down based on business needs

|

|

Expertise

|

Limited to one person’s knowledge

|

Access to a team of specialists with industry expertise

|

|

Security

|

Data stays in-house, but security depends on internal protocols

|

Secure cloud-based systems with encryption and compliance measures

|

Frequently Asked Questions

What is the difference between accounts payable and accounts receivable in terms of cash flow?

+On the cash flow statement, AP increases represent a cash inflow (you received something of value without paying yet), while AP decreases represent outflows (you paid). For AR, increases represent a use of cash (you gave away value without receiving cash), while AR decreases represent cash inflows (you collected payment). Managing the timing of these flows determines whether a business can comfortably meet its obligations each month.

What is the main difference between accounts payable and accounts receivable?

+Accounts payable is money your business owes to vendors and suppliers for goods or services received on credit. Accounts receivable is money customers and clients owe your business for goods or services you have already delivered on credit. AP is a liability; AR is an asset.

Can the same transaction appear in both AP and AR?

+Not within the same company's books for the same transaction. However, the same business transaction creates an AR entry for the seller and an AP entry for the buyer. Two different companies record the same invoice in different ways depending on which side of the transaction they are on.

Is accounts receivable a debit or credit?

+Accounts receivable is debited when created (increasing the asset account) and credited when the customer pays (reducing the asset account). It carries a normal debit balance, consistent with its classification as a current asset.

How does accounts payable affect my credit rating?

+Consistently paying AP on time, or early, builds a positive credit history with suppliers and lenders. Late AP payments can lead to penalties, loss of early payment discounts, damaged supplier relationships, and in some cases can be reported to business credit bureaus, affecting your ability to access trade credit in the future.