Let me describe a situation you have probably lived through; you check your bank balance online and see a healthy number, so you feel good about paying that vendor invoice or buying new equipment. Then you open your accounting software later that same day, and the number there tells a completely different story.

Now you have two versions of your cash position, no idea which one is right, and a decision to make before the end of the day.

That feeling of not knowing which number to trust is exactly why bank reconciliation exists. It is a simple, methodical process that compares your bank statement against your internal records and explains every single difference between them. By the time you finish reading this guide, you will know how to run a reconciliation from start to finish, you will see a real example with actual numbers, and you will understand the common mistakes that cause most reconciliations to fail. More importantly, you will never have to guess your cash balance again.

Key Takeaways

- Bank reconciliation matches your internal records against your bank statement and explains every single difference between them.

- Differences almost always come from timing issues (checks that haven’t cleared, deposits in transit), missed entries (bank fees, interest), or human errors.

- A completed reconciliation gives you your true cash position so you stop guessing which balance is right.

- Regular reconciliations catch small mistakes before they turn into audit problems, fraud losses, or bad business decisions.

What Is a Bank Reconciliation?

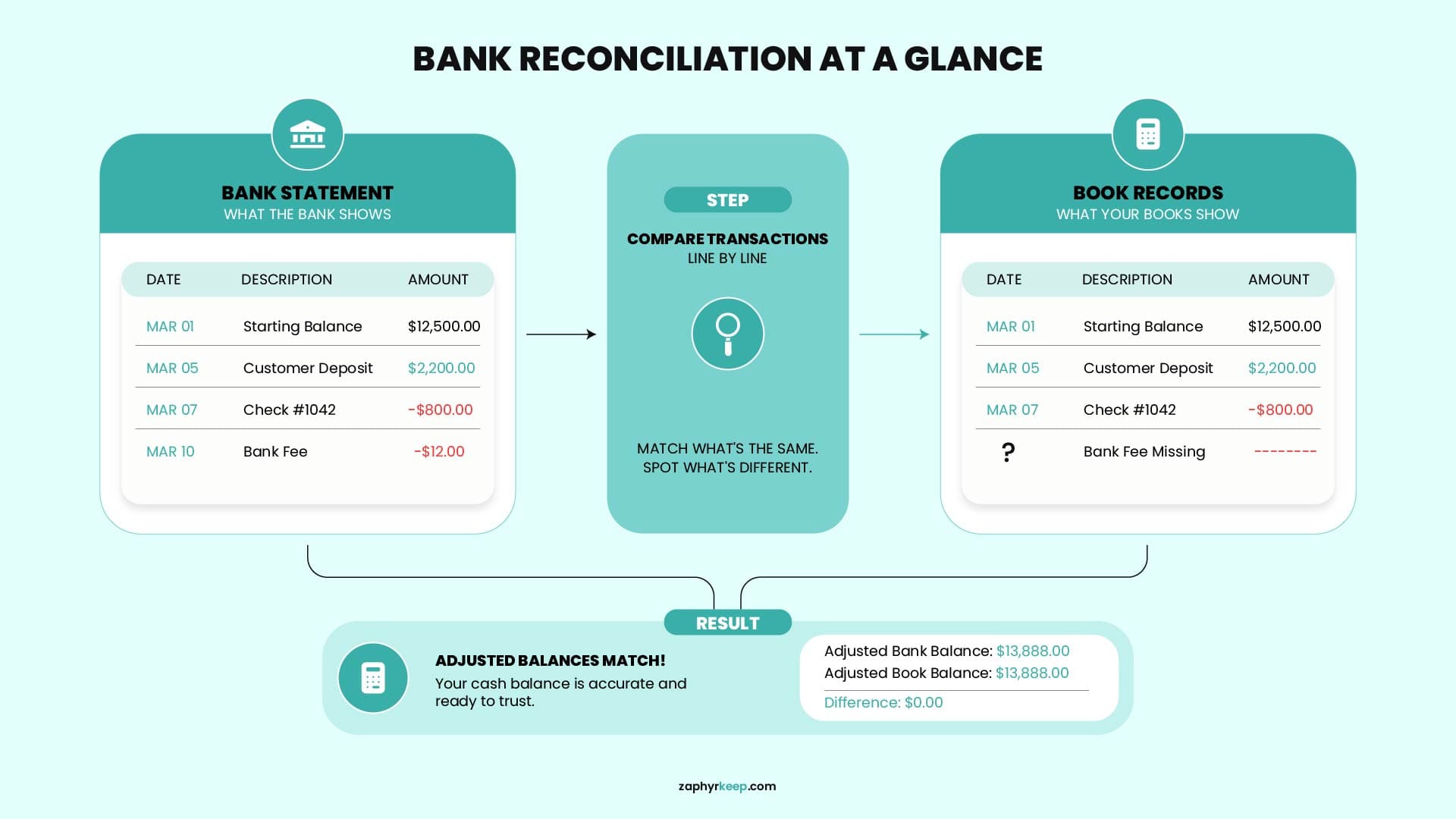

So to answer what is a bank reconciliation, you take your bank statement and your internal financial records, then compare every transaction line by line. You match deposits, checks, electronic payments, and fees. Every difference gets investigated and explained and when you finish, both balances agree and you know your true cash position.

Now here is the formal definition for when someone asks: a bank reconciliation is an accounting process of matching what appears on your bank statement with what appears in your accounting records, then identifying and explaining anything that doesn’t line up. The whole point is to confirm that your cash balance is correct, not just assume it’s.

Why Is Bank Reconciliation Important for Your Business?

Finance teams spend between thirty and forty percent of their time on manual matching tasks, according to PwC data cited by Open Ledger. To put that in perspective, nearly two full days out of every workweek are spent matching transactions instead of doing work that actually helps the business grow.

Here is another interesting fact worth paying attention to. Konica Minolta had days sales outstanding stuck at 69 days, with barely three percent of customer payments applying automatically. Millions of dollars were just sitting there completely locked up in cash flow they could not access or use for anything productive. After the company finally fixed their reconciliation and payment processes, they cut days sales outstanding by nine days and unlocked thirty million dollars in cash. That is thirty million dollars that was trapped simply because their bank reconciliation process was too slow and inefficient.

These two facts tell you everything you need to know about why bank reconciliation matters for your business. This isn’t about checking a meaningless box at the end of every month but more about knowing exactly how much cash you actually have available, catching small errors before they turn into much bigger problems, and spotting fraudulent transactions before someone drains your account dry without you noticing.

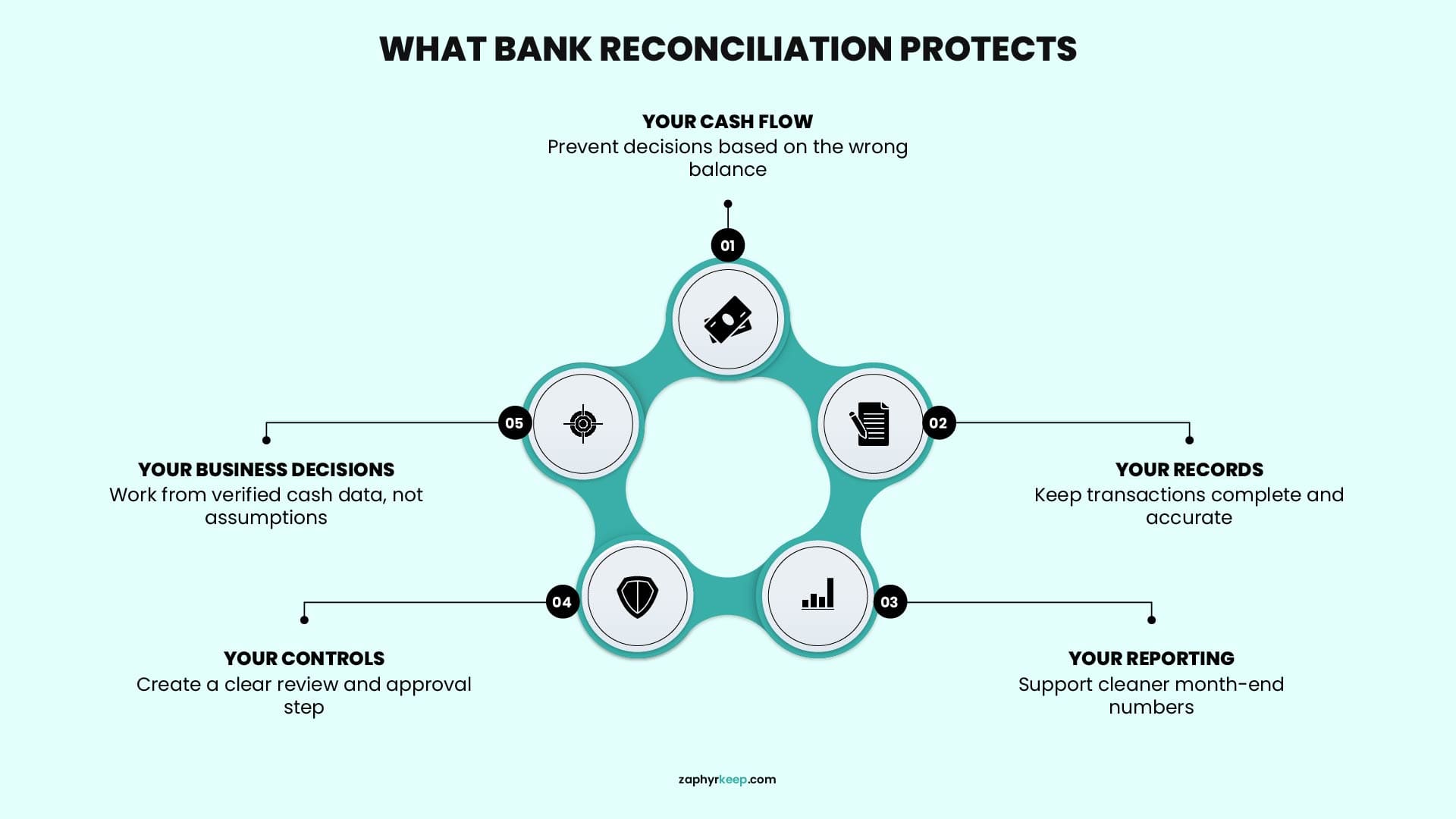

Let me walk you through what bank reconciliation actually does for your business.

Cash accuracy – When you run your bank reconciliation steps on a regular schedule, you stop guessing which balance is the right one. You simply know the answer because you did the work to verify it. That means you can pay your vendors on time, run payroll without sweating through it every two weeks, and invest in new inventory or equipment because you trust the number sitting right in front of you.

Error detection – Bank errors are relatively rare, but they do happen from time to time. A check clears for the wrong dollar amount. A deposit gets posted to your account twice. More often than not though, the error comes from your side of the equation. You type 530 instead of 350. You accidentally record the same payment twice. A good bank reconciliation guide will tell you that running regular reconciliations catches every single one of these mistakes.

Fraud prevention – This is the benefit that most business owners do not think about until it is already too late. The Association of Certified Fraud Examiners found that account reconciliation catches approximately five percent of all occupational fraud cases, which adds up to millions of dollars in detected fraud every year. Learning how to do a bank reconciliation properly forces suspicious transactions into the light because they will never match anything in your internal records.

Clean reporting – Your tax preparer, your bank lender, and your potential investors all want to see accurate financial statements. Those statements come directly from your books and records. If your books are wrong because you never reconciled them against your bank statements, then every single report built on top of those books is wrong too.

Stronger controls – When you perform bank reconciliations every single month without fail, you build a lasting habit of accountability throughout your organization. Someone reviews every transaction that hits your accounts. Someone questions every discrepancy that appears and that alone discourages careless mistakes and makes fraudulent activity much harder to hide from view.

Bank Statement vs. Your Books: Understanding the Differences

When your bank balance and your book balance do not match, the difference usually falls into one of three buckets: timing, bank activity, or recording errors. Once you know which bucket you are dealing with, the rest of your bank reconciliation steps become completely clear instead of frustrating.

Here is how each bucket works and what you actually need to do.

Timing Differences

|

Type

|

What Is Happening

|

Action Needed

|

|---|---|---|

|

Outstanding checks

|

You recorded a check in your books, but the recipient has not cashed it yet. Your books show the money gone. The bank does not.

|

Wait for the check to clear.

|

|

Deposits in transit

|

You recorded a deposit, but the bank has not finished processing it. Your books show the money received. The bank does not.

|

Wait for the bank to process it.

|

|

Transaction timing

|

You initiated a payment on the last day of the month. Your books record it in the current month. The bank processes it the following month.

|

No action needed. Both are correct.

|

|

Card settlements

|

A customer paid by credit card. Your books show the sale immediately. The bank takes two to three days to settle and deposit the funds.

|

Wait for the settlement to appear.

|

Bank-Only Entries

|

Type

|

What Is Happening

|

Action Needed

|

|---|---|---|

|

Bank fees

|

The bank charged a fee for maintenance, wires, or overdrafts. Your books have no record of it.

|

Record the fee as an expense. Reduce your cash balance.

|

|

Interest income

|

The bank paid you interest on your balance. Your books do not show this income.

|

Record the interest as income. Increase your cash balance.

|

|

Direct debits

|

A vendor pulled money automatically from your account. Your books may have missed this recurring payment.

|

Record the direct debit as an expense.

|

|

Returned payments (NSF)

|

A customer check bounced after you already recorded it as a deposit. The bank reversed the transaction.

|

Reverse the deposit in your books. Bill the customer again.

|

|

Chargeback fees

|

A customer disputed a credit card charge. The bank deducted the disputed amount plus a processing fee.

|

Record the chargeback as a reduction in revenue. Record the fee as an expense.

|

|

Wire transfer fees

|

You sent or received a wire transfer. The bank charged a fee that appears only on the statement.

|

Record the fee as an expense.

|

Recording Errors

|

Type

|

What Is Happening

|

Action Needed

|

|---|---|---|

|

Data entry mistakes

|

You typed 540 instead of 450. You missed a transaction entirely. You recorded it to the wrong vendor.

|

Correct the wrong entry. Add the missing entry.

|

|

Duplicate entries

|

You recorded the same transaction twice by accident. The bank shows only one.

|

Delete the duplicate entry. Keep the original.

|

|

Wrong account classification

|

You recorded a payment as office supplies when it should be equipment purchase. The dollar amount is correct.

|

Change the account category. The cash balance stays the same.

|

|

Reversed signs

|

You added a deposit as positive when it should be a withdrawal, or vice versa.

|

Flip the sign. Add what should be subtracted.

|

How to Do a Bank Reconciliation Step by Step

People searching for “how to reconcile a bank statement” or “bank reconciliation steps” usually expect a complicated accounting procedure and steps, but the reality is different. Here is the exact basic process you need to follow, whether you do it manually or with software.

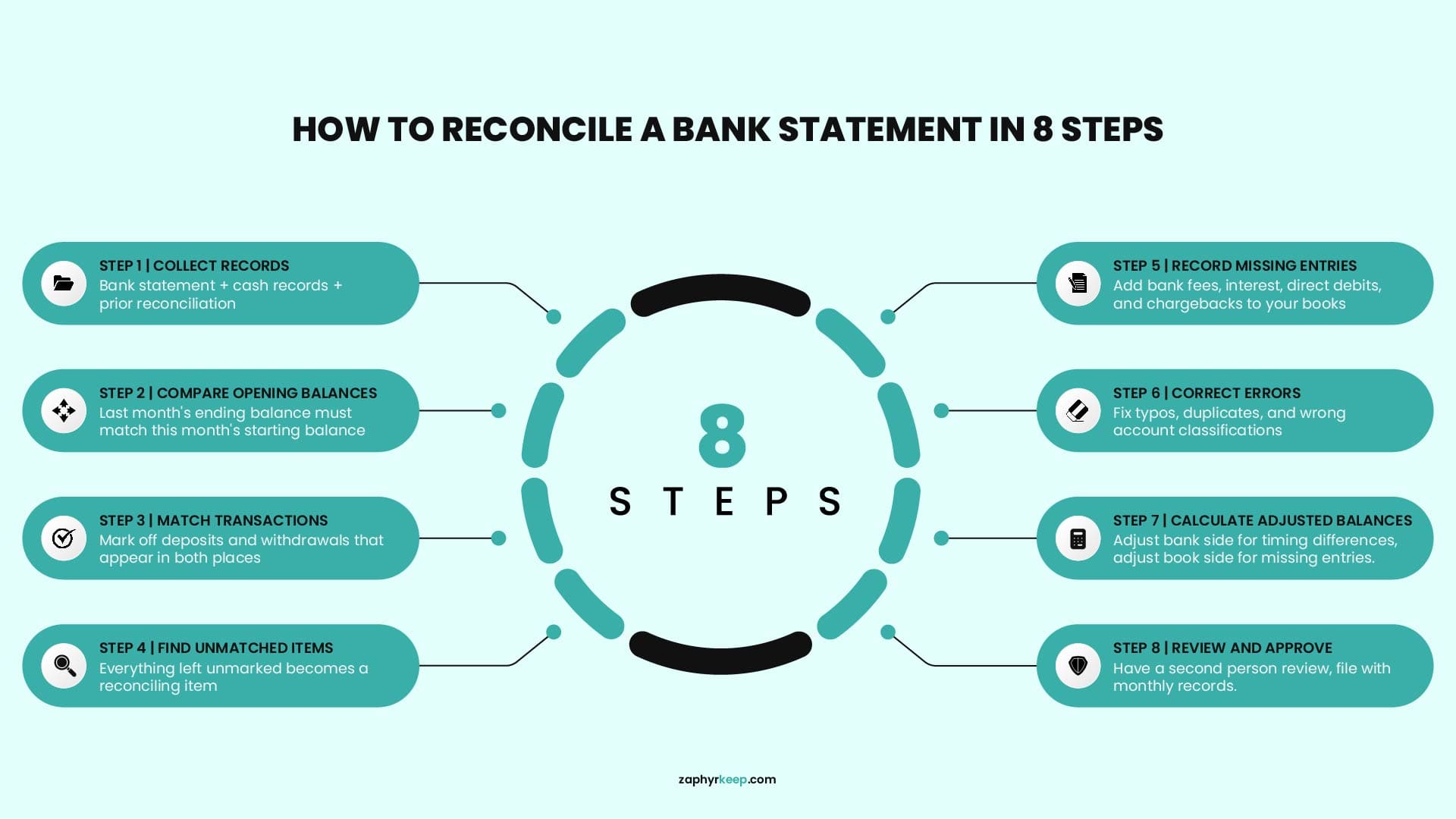

Step 1: Collect your records

Grab your bank statement for the period you are reconciling and your internal cash records (general ledger or accounting software report). Also keep last month’s reconciliation handy to verify your opening balances.

|

Factor

|

In-House Bookkeeping

|

Outsourced Bookkeeping

|

|---|---|---|

|

Cost

|

Salaries, benefits, training, and software costs add up

|

Pay for services as needed, often cheaper in the long run

|

|

Control

|

Direct oversight, instant access to financial data

|

Less control, but reports and updates are scheduled

|

|

Scalability

|

Hiring new staff is expensive and time-consuming

|

Scale services up or down based on business needs

|

|

Expertise

|

Limited to one person’s knowledge

|

Access to a team of specialists with industry expertise

|

|

Security

|

Data stays in-house, but security depends on internal protocols

|

Secure cloud-based systems with encryption and compliance measures

|

Step 2: Compare opening balances

Check that the beginning balance on this month’s bank statement matches the ending balance from your prior reconciliation. If these numbers do not line up, stop and investigate before moving forward.

Step 3: Match transactions

Go line by line through deposits and withdrawals. Mark off every transaction that appears in both your bank statement and your books. Work from largest amounts to smallest. This saves time because big transactions are easier to spot and match.

Step 4: Find unmatched items

Anything that remains unmarked after Step 3 becomes a reconciling item. List these separately. Some will be timing differences like outstanding checks or deposits in transit. Others will be missing entries or errors.

Step 5: Record missing entries

Look at your list of unmatched items. For bank fees, interest income, direct debits, or chargebacks that appear only on the bank statement, add these transactions to your books now. Your bank already knows about them. Your books need to catch up.

Step 6: Correct errors

For data entry mistakes, duplicate entries, or wrong account classifications, fix them directly in your books. If you typed 540 instead of 450, change the number. If you recorded the same payment twice, delete the duplicate.

Step 7: Calculate adjusted balances

Take your bank statement balance. Add any deposits in transit. Subtract any outstanding checks. This gives you your adjusted bank balance. Now take your book balance. Add any interest income or missing deposits. Subtract any bank fees or returned payments. This gives you your adjusted book balance. Both adjusted numbers should now match.

Step 8: Review and approve

Have someone who was not involved in the reconciliation review your work. A second pair of eyes catches mistakes you might have missed. Once approved, file the reconciliation with your monthly records for audit purposes.

Bank Reconciliation Example

Let us walk through a real example, suppose an ABC Consulting runs their March reconciliation with the following starting numbers.

|

Item

|

Amount

|

|---|---|

|

Bank statement balance (March 31)

|

$25,000

|

|

Book balance (March 31)

|

$24,420

|

The difference is $580. Here is what caused it.

|

Reconciling Item

|

Impact on Bank Side

|

Impact on Book Side

|

|---|---|---|

|

Deposit in transit (customer payment)

|

+ $2,000

|

-

|

|

Outstanding checks (two unpaid vendor checks)

|

- $1,500

|

-

|

|

Bank service fee

|

-

|

- $50

|

|

Interest earned

|

-

|

+ $30

|

Now calculate both adjusted balances.

|

Calculation

|

Amount

|

|---|---|

|

Bank balance

|

$25,000

|

|

Add: Deposit in transit

|

+ $2,000

|

|

Less: Outstanding checks

|

- $1,500

|

|

Adjusted bank balance

|

$25,500

|

|

Calculation

|

Amount

|

|

Book balance

|

$24,420

|

|

Less: Bank service fee

|

- $50

|

|

Add: Interest earned

|

+ $30

|

|

Add: Missing customer payment (found during reconciliation)

|

+ $1,100

|

|

Adjusted book balance

|

$25,500

|

Both adjusted balances now match at $25,500. The reconciliation is complete.

Common Bank Reconciliation Mistakes to Avoid

Most bank reconciliation mistakes are not dramatic. They usually come from small habits that make the process weaker and the final cash balance less reliable, like:

- Delaying the reconciliation

The longer you wait, the harder it becomes to trace what happened. A $48 bank charge from last week is easier to explain than one buried three months back as delays create backlog, so one unresolved item can keep rolling forward.

- Ignoring small differences

A $12 mismatch may not feel urgent, but it still means something is wrong. It could be a missed fee, a duplicated payment, or a transaction entered as $540 instead of $450 as small errors often point to bigger process issues.

- Working without complete documentation

A proper bank reconciliation process needs support behind it. If statements, receipts, or payment records are missing, you cannot verify the difference with confidence. At that point, you are relying on memory instead of evidence.

- Posting unsupported adjustments

One of the worst habits is forcing the numbers to match with a vague correction. If you add a $275 adjustment just to close the gap, but cannot explain where it came from, the reconciliation is not actually complete.

- Skipping the review step

Even if one person prepares the reconciliation, someone should still review it. A second look can catch a reversed number, a missing fee, or an old outstanding item that should not still be there.

- Mixing personal and business transactions

If a personal $95 grocery charge lands in the business account, it creates confusion immediately. It also makes the reconciliation harder and weakens the quality of your financial records.

- Not clearing old outstanding items

Checks or deposits should not stay outstanding forever. If a $1,200 check is still showing as uncleared after two months, it needs to be investigated. It may have been lost, voided, or recorded incorrectly.

- Reconciling to the wrong period

If your bank statement covers June 1 to June 30, but your books include July transactions, the balances will not line up properly. Always reconcile using the same cutoff date on both sides.

Who Should Perform and Review Bank Reconciliations?

Now comes an important question: who should actually handle bank reconciliations? A lot of business owners assume this has to stay on their desk but in reality it depends on your transaction volume, how your team is structured, and whether there is someone who can properly review the work, for example:

The owner

If the business has a low number of transactions and the records are straightforward, the owner can handle the reconciliation. That usually works when activity is still manageable and there is enough time to review each item carefully. The problem starts when reconciliations become rushed, inconsistent, or pushed to the end of the month because other priorities take over.

A bookkeeper

In most growing businesses, this is the best person to prepare reconciliations. A good bookkeeper works through the transactions regularly, records missing items, clears old differences, and keeps the cash balance accurate before month-end reporting begins.

An accountant

An accountant is better used as a reviewer than as the person matching every transaction line by line. Their value is in spotting weak explanations, unusual adjustments, or control issues that need attention, not in spending time on routine transaction matching.

Preparer vs reviewer

These roles should stay separate whenever possible; as the preparer handles the reconciliation, documents each difference, and makes sure the supporting records are in place. The reviewer then checks the work, questions anything unclear, and approves the final balance. That separation strengthens the process and makes it easier to catch errors or unusual transactions before they slip through.

If you do not have someone internally who can review the work, consider outside help. Many small business owners find that learning when to outsource bookkeeping in 2026 is the difference between staying stuck in the weeds and finally getting their time back.

Should You Do Bank Reconciliations Manually or Use Software?

Here’s some interesting number to share, businesses using automated reconciliation tools complete their reconciliations 85% faster than those doing it manually. That is the difference between spending your Friday afternoon matching transactions and being done before lunch.

Manual process (pen and paper)

You print your bank statement, pull out your checkbook register, and go line by line with a highlighter. This works if you have maybe ten to twenty transactions per month, but beyond that it becomes painful fast and errors become much more likely.

Spreadsheet process (Excel or Google Sheets)

You download your bank statement and use formulas to help match transactions. This is better than paper, but spreadsheets do not automatically flag duplicates or missing entries. According to one finance professional’s estimate, the average small business owner spends 80+ hours per year on bookkeeping tasks, and a large chunk of that time goes straight to reconciliation.

Software-assisted process (QuickBooks, Xero, or dedicated tools)

Accounting software connects directly to your bank feed and automatically matches most transactions for you. Your job shifts from matching everything to reviewing the few exceptions. The global accounting software market hit $26.95 billion in 2025 and continues growing, which tells you that businesses are voting with their wallets.

When to switch. If you are spending more than two hours per month on reconciliations or managing multiple accounts, software will pay for itself in time saved. Once your business grows past the hobby stage, software is not a luxury anymore. It is a necessity.

Conclusion

Time to wrap things up. Your bank balance and your books are not going to match on their own, and crossing your fingers every month is not exactly a financial strategy. Regular reconciliation takes the guesswork out of your cash position, catches small mistakes before they turn into big headaches, and hands you real numbers you can actually trust when making decisions about payroll, inventory, or that new hire you have been thinking about.

If you are tired of spending your weekends chasing down discrepancies that should not even be there in the first place, ZaphyrKeep works with small and mid-sized businesses across the US to handle reconciliations and keep books clean month after month without you having to think about it.

Reach out to the team and see what it looks like when someone else handles the numbers for a change. You might actually enjoy your next month end.

Frequently Asked Questions

What is a bank reconciliation in simple terms?

+A bank reconciliation is the process of matching your bank statement with your accounting records to ensure both balances are accurate and explain any differences.

Is bank reconciliation part of the double-entry system?

+No, the bank reconciliation statement is not part of the double-entry bookkeeping system. It is a separate process used to verify and explain differences between your cash book balance and your bank statement balance. Think of it as a verification tool rather than an accounting entry

How often should you do a bank reconciliation?

+At a minimum, once a month, usually at the end of each statement period. If your business handles frequent transactions, weekly or even daily bank reconciliations are more effective. This helps you catch errors early, clear outstanding items faster, and avoid delays during month-end closing and reporting.

What is the difference between bank reconciliation and cash reconciliation?

+Bank reconciliation focuses on one account, where you check that your bank balance matches your books. Cash reconciliation, on the other hand, is broader. It looks at all your cash, including bank accounts, petty cash, and other balances, to make sure everything adds up correctly.

What is an example of a bank reconciliation adjustment?

+Common adjustments include bank fees, interest income, or a deposit recorded in your books but not yet processed by the bank.