Introduction

Bookkeeping isn’t just about keeping track of numbers—it’s what keeps your business running smoothly. When done right, it helps manage cash flow, meet tax deadlines, and keep financial records accurate. Without it, things can get messy fast.

But here’s the big question: Should you handle bookkeeping yourself, or is it better to outsource?

Some business owners like to keep it in-house because it gives them full control and direct access to their financial data. Others prefer outsourcing to save time, cut costs, and get expert help without hiring a full-time employee.

Both choices have their pros and cons. The right one for you depends on your business size, budget, and future plans.

In this read, we’ll break down the benefits, drawbacks, and costs of both options to help you decide what’s best for your business. By the end, you’ll know which approach makes the most sense for your financial needs.

What is In-House Bookkeeping?

In-house bookkeeping means handling your business’s financial records on your own, rather than outsourcing them to a third party. This can be done in a few ways—you might hire a dedicated bookkeeper, give the task to an existing employee, or even manage it yourself as the business owner.

Many small businesses start by doing their own bookkeeping, but as transactions grow, so does the need for accuracy and compliance. That’s when hiring a bookkeeper becomes a smarter move.

A survey by Clutch found that 60% of small businesses manage bookkeeping in-house, but many struggle because they don’t have the specialized financial knowledge needed to do it efficiently.

How In-House Bookkeeping Works

An in-house bookkeeper is responsible for tracking daily financial transactions, reconciling accounts, managing payroll, processing invoices, and ensuring tax compliance. Since they work directly within the company, they have a hands-on approach to financial management and can provide immediate financial insights.

However, this also comes with added responsibilities, such as hiring, training, and maintaining an internal bookkeeping system.

Common Tools and Software Used

To handle bookkeeping efficiently, businesses use accounting software such as QuickBooks, Xero, FreshBooks, and Zoho Books. These platforms help with expense tracking, financial reporting, tax preparation, and payroll management.

While they simplify bookkeeping, businesses must ensure proper training and regular updates to comply with tax regulations and financial reporting standards.

What is Outsourced Bookkeeping?

Bookkeeping is essential, but let’s be honest—not every business wants to handle it in-house.

Outsourced bookkeeping means bringing in an external professional or service to manage your financial records, rather than hiring a full-time employee.

It’s a popular choice for businesses that want to save time, cut costs, and tap into expert financial knowledge without the hassle of managing bookkeeping themselves.

Many businesses choose outsourcing because it’s more flexible and cost-effective than keeping things in-house. A study by QuickBooks found that small businesses that outsource bookkeeping save an average of 50% compared to hiring a full-time bookkeeper.

Instead of paying a salary, benefits, and software costs, you only pay for the services you actually need—which can be a game-changer for small and growing businesses. Isn’t it?

How Outsourced Bookkeeping Works

When you opt for outsourcing bookkeeping, you hand over financial tracking, transaction recording, bank reconciliations, payroll processing, and tax preparation to an external provider. Most of the work is done remotely using cloud-based accounting software, so you can still access your financial data whenever you need it.

Some bookkeeping firms even provide monthly financial statements and tax-ready reports, so you don’t have to stress about compliance.

Types of Outsourced Bookkeeping

Not all outsourcing bookkeeping services are the same. Businesses can choose from different options based on their needs and budget:

- Freelance Bookkeepers – If your business has simple financial needs, you can hire an independent bookkeeper on a contract basis. This is an affordable way to get professional support without committing to a full-time hire.

- Accounting Firms – For businesses with more complex financial requirements, an accounting firm offers a team of experts who handle everything from bookkeeping to tax strategy and compliance.

- Cloud-Based Bookkeeping Services – Online bookkeeping platforms combine automation and professional support, offering real-time financial tracking, AI-driven analytics, and easy integrations with your existing systems.

Common Tools and Software Used

Most outsourcing bookkeeping services rely on cloud-based accounting software to keep things running smoothly. Popular platforms like QuickBooks Online, Xero, FreshBooks, and Bench allow businesses to automate invoicing, track expenses, manage payroll, and generate reports in real-time.

Since everything is stored in the cloud, business owners can access their financial data anytime, from anywhere.

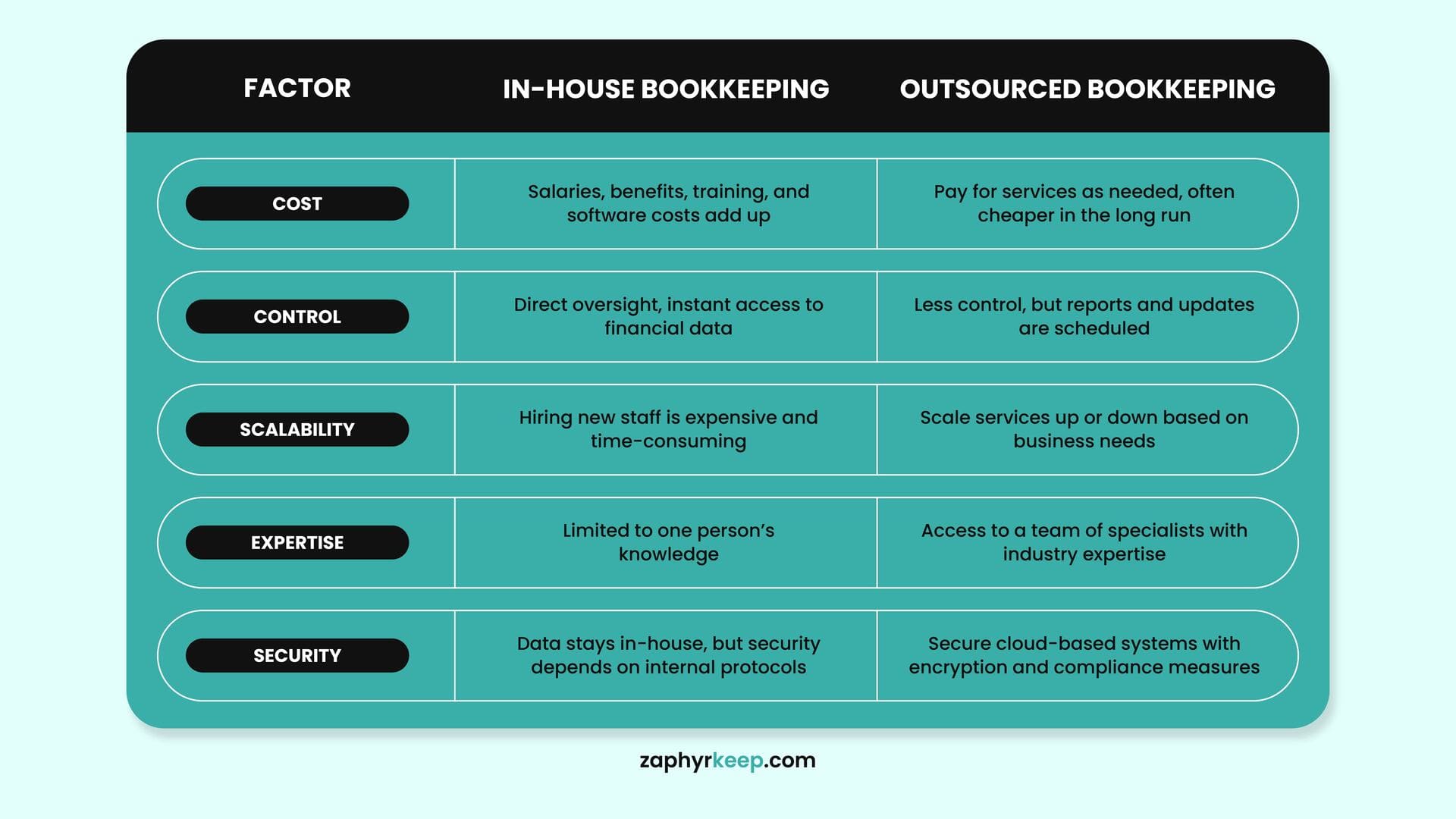

Key Differences Between Outsourced and In-House Bookkeeping

Managing bookkeeping in-house gives businesses full control over their financial data but comes with higher costs. Outsourcing, on the other hand, reduces overhead and provides access to expert support, but it requires trust in an external provider.

However, cost and control aren’t the only factors—scalability, expertise, and security also play a crucial role in determining the best approach.

The table below outlines the key differences between in-house and outsourced bookkeeping, helping you assess which option aligns best with your business needs.

|

Factor

|

In-House Bookkeeping

|

Outsourced Bookkeeping

|

|---|---|---|

|

Cost

|

Salaries, benefits, training, and software costs add up

|

Pay for services as needed, often cheaper in the long run

|

|

Control

|

Direct oversight, instant access to financial data

|

Less control, but reports and updates are scheduled

|

|

Scalability

|

Hiring new staff is expensive and time-consuming

|

Scale services up or down based on business needs

|

|

Expertise

|

Limited to one person’s knowledge

|

Access to a team of specialists with industry expertise

|

|

Security

|

Data stays in-house, but security depends on internal protocols

|

Secure cloud-based systems with encryption and compliance measures

|

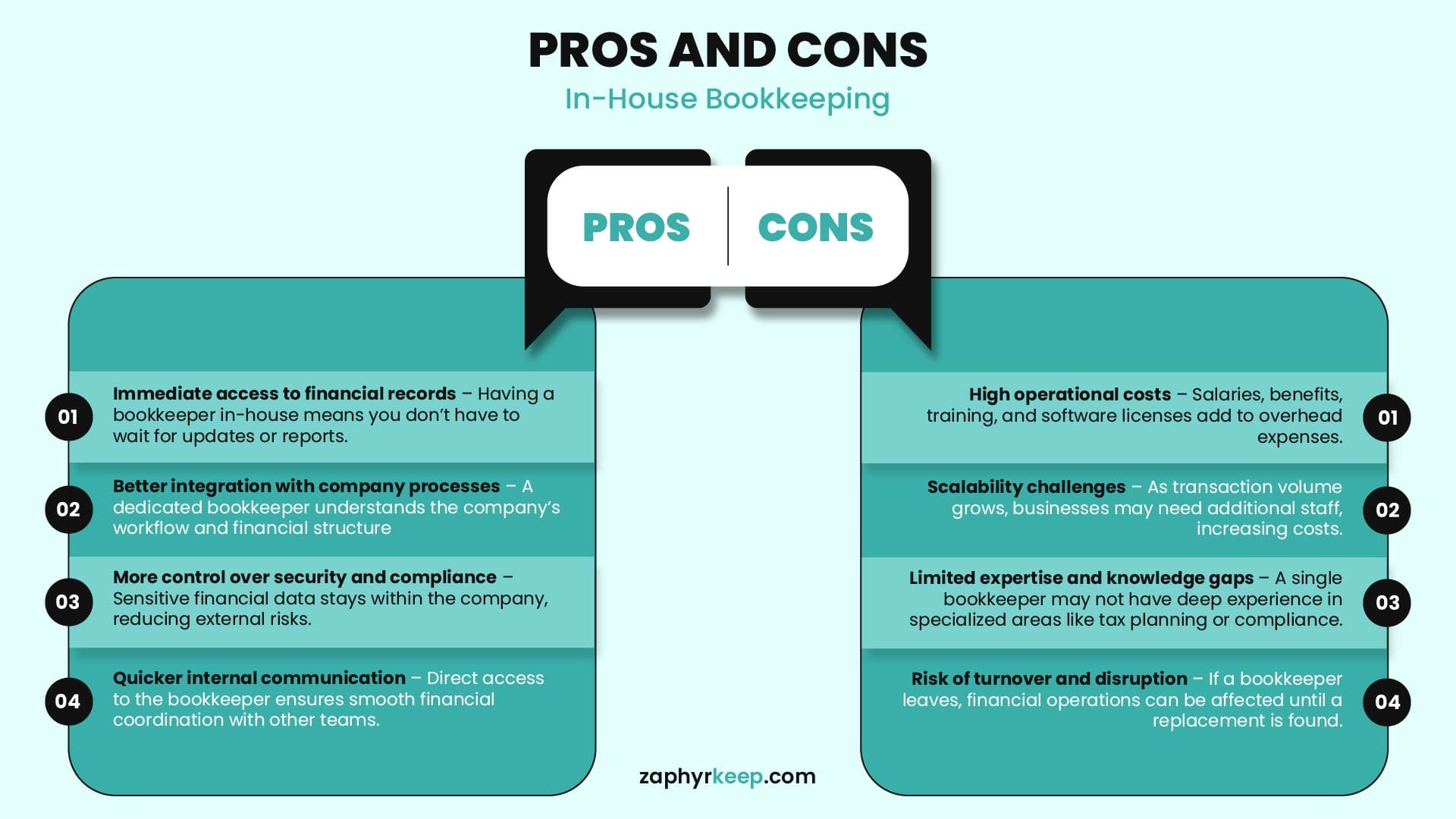

Pros and Cons of In-House Bookkeeping

In-house bookkeeping is ideal for businesses that want direct oversight of their financial operations. Having a bookkeeper on staff means instant access to records, personalized financial management, and better coordination with other departments.

However, this approach comes with higher costs, training requirements, and limited scalability. Many businesses struggle with keeping up-to-date with regulatory changes, tax laws, and financial best practices, especially when relying on a small internal team.

The infographic below highlights the key pros and cons of in-house bookkeeping for quick comparison.

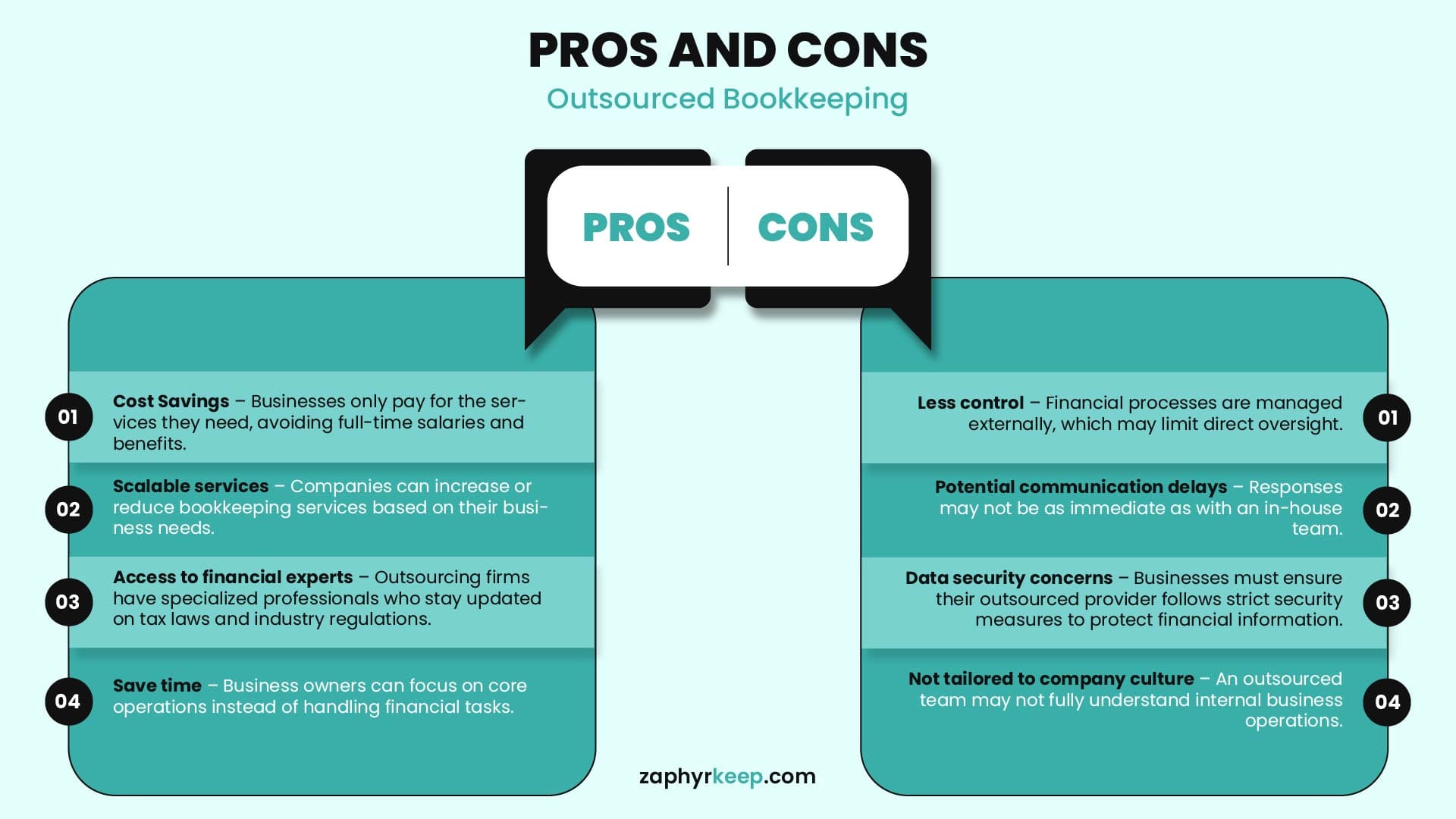

Pros and Cons of Outsourced Bookkeeping

Outsourced bookkeeping allows businesses to delegate financial tasks to external professionals, reducing the workload on internal teams. This option is cost-effective, scalable, and gives access to experienced bookkeepers without the commitment of hiring full-time staff.

However, outsourcing also means less direct control over financial operations and requires trusting a third party with sensitive business data.

For companies that prioritize efficiency and cost savings, outsourcing bookkeeping can be a practical solution.

The following visual highlights the key pros and cons of outsourcing bookkeeping.

When to Choose In-House Bookkeeping

In-house bookkeeping is best for businesses that require direct control over financial operations and deal with high transaction volumes or strict industry regulations. Industries like healthcare, finance, and legal services often manage bookkeeping internally to ensure compliance and data security.

However, handling bookkeeping in-house demands significant time. A report by Starling Bank found that micro-businesses spend 15 hours per week on financial admin, which can take focus away from core business activities (Accountancy Age).

While this approach offers immediate access to financial records, it also involves higher costs for salaries, training, and software. Businesses must assess whether they have the resources to maintain an internal team without impacting overall efficiency.

When to Choose Outsourced Bookkeeping

Outsourced bookkeeping is ideal for businesses looking to cut costs and access financial expertise without hiring full-time staff. Small and medium-sized businesses benefit the most, as 37% of small businesses outsource accounting and IT services to improve efficiency.

This option is also great for fast-growing or seasonal businesses that need scalable bookkeeping support. Retailers, for example, can adjust bookkeeping services during peak seasons without hiring extra staff. Startups, too, gain professional financial management from the start, allowing founders to focus on growth.

While outsourcing reduces administrative burden, businesses must ensure data security and compliance when choosing a provider. Weighing cost savings against control over financial processes is essential before making the switch.

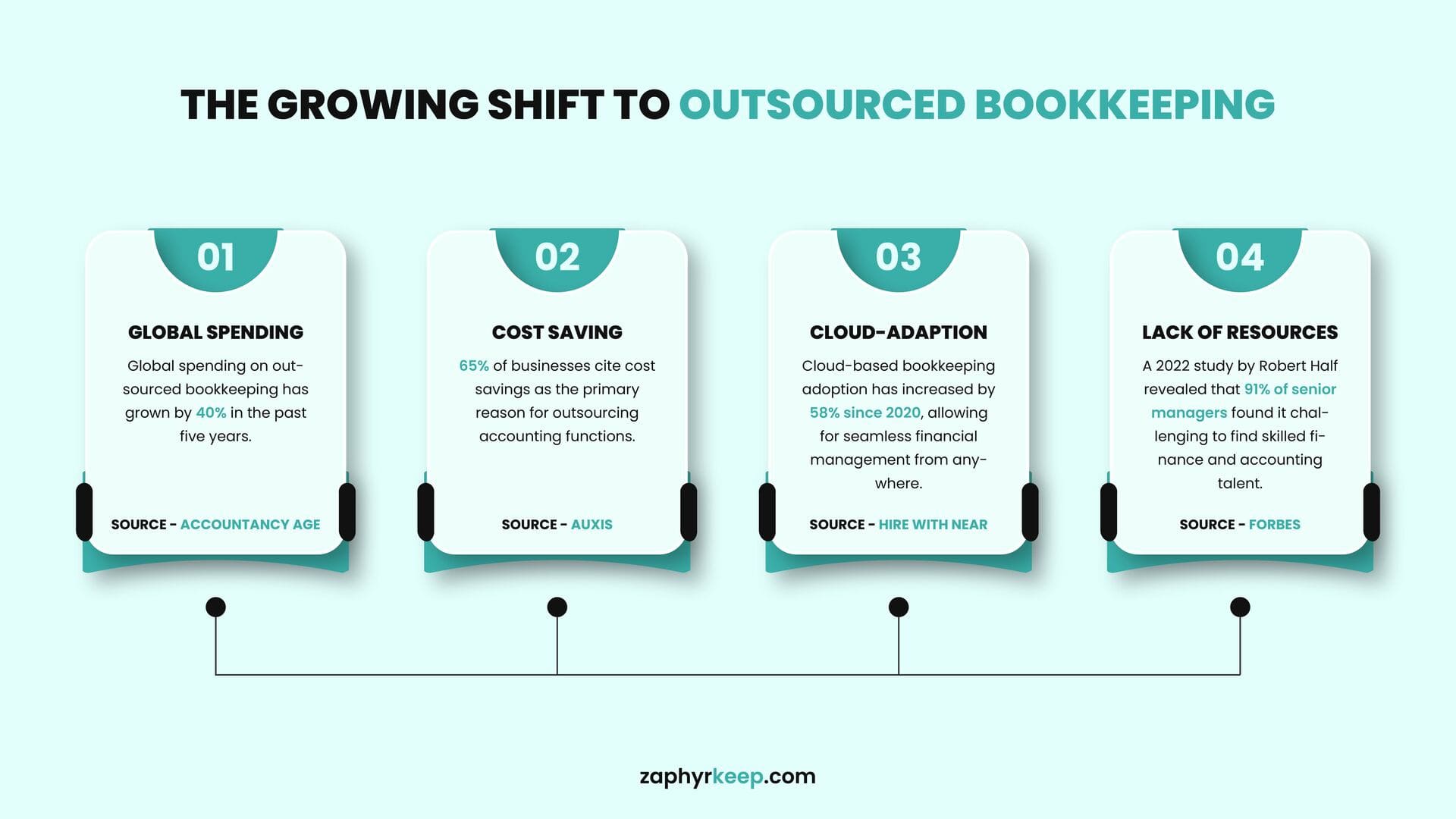

Trends in Bookkeeping: The Shift to Outsourcing

More businesses are outsourcing bookkeeping than ever before, driven by cost savings, technology, and the growing demand for financial expertise. Over the past five years, global spending on outsourced accounting has increased by nearly 40% (Accountancy Age). Cloud-based technology and automation tools have also made it easier than ever to work with remote bookkeeping professionals, ensuring real-time access to financial data without hiring in-house staff.

The following visual highlights the key trends shaping bookkeeping and why outsourcing is becoming the preferred choice.

How to Decide What’s Best for Your Business

Deciding between in-house and outsourced bookkeeping depends on cost, efficiency, and financial goals. If your business requires constant access to financial data and has the budget for a dedicated team, in-house bookkeeping may be the right fit. However, 59% of businesses outsource to cut costs (Deloitte Global Outsourcing Survey), making it a popular option for companies looking to reduce expenses while maintaining accuracy.

Fast-growing businesses benefit from outsourcing due to its flexibility, while industries with strict compliance requirements, like healthcare and finance, often prefer in-house bookkeeping. Evaluating budget, scalability, compliance, and expertise needs will help determine the best approach.

Final Thoughts

So, what’s the best way to handle your bookkeeping? Should you keep it in-house for full control, or does outsourcing make more sense?

By now, you should have a clear idea of which option best suits your business. But just to recap:

- In-house bookkeeping gives you full control and instant access to financial data. It’s a good fit if you have the time, expertise, and resources to manage it effectively.

- Outsourcing saves time, lowers costs, and provides expert support—without the hassle of hiring and training an internal team.

Both options have their pros and cons, and the right choice depends on your business size, budget, and long-term goals. Ultimately, the best approach is the one that ensures accuracy, efficiency, and financial stability for your business.