You started your business to do the work you’re good at. Not to spend Sunday evenings reconciling bank accounts, hunting for missing receipts, or trying to figure out why your numbers don’t match. But that’s where a lot of small business owners end up, and the longer it goes on, the harder it gets to climb out.

Doing your own bookkeeping doesn’t actually save money. It costs time you could spend growing the business, accuracy you can’t afford to lose, and mental energy that should go toward decisions that actually move the needle.

This guide covers everything you need to know before you make a move. What outsourced bookkeeping actually is, how to tell if you need it, what it costs, how to do it right, and which mistakes to avoid so you don’t end up starting over three months in.

What Is Outsourced Bookkeeping?

Outsourced bookkeeping means hiring an outside person or company to manage your financial records instead of doing it yourself or keeping someone on payroll. They track your income and expenses, reconcile your bank accounts, manage your payroll records, and send you clean financial reports every month. You keep full access to your books at all times, but the work of maintaining them is no longer yours to carry.

This isn’t a new concept, but it’s become far more practical for small businesses over the last several years. Cloud-based tools like QuickBooks Online, Xero, and FreshBooks let a remote bookkeeper work inside your accounts in real time without ever stepping into your office.

You share access to your bank feeds and credit card accounts, they do the work, and you get organized reports at month end. Some providers check in weekly. Others work quietly in the background and deliver everything on a set schedule. The right cadence depends on your business and how much communication you actually want.

Is It the Same as Hiring an Accountant?

No, and this distinction trips up a lot of business owners.

A bookkeeper records and organizes your financial transactions on an ongoing basis. An accountant takes that organized data and uses it to prepare your taxes, provide financial advice, and handle more complex compliance work. Think of it this way: the bookkeeper builds the foundation, and the accountant works from it.

You typically need both, but they serve different purposes at very different price points. A good CPA in the US charges anywhere from $150 to $400 per hour according to the American Institute of CPAs. When they spend the first two hours of your engagement sorting through a year of disorganized records, you pay for every minute of that time.

When your books arrive already clean and reconciled, your accountant focuses on tax strategy and advice instead of cleanup. That difference alone tends to save small business owners hundreds of dollars per year in accounting fees.

Signs It's Time to Outsource Your Bookkeeping

Before you make any decisions, you need an honest look at where you actually stand. Some businesses don’t need outside help yet. Others needed it six months ago and just haven’t acted. These are the signs that point toward it being time.

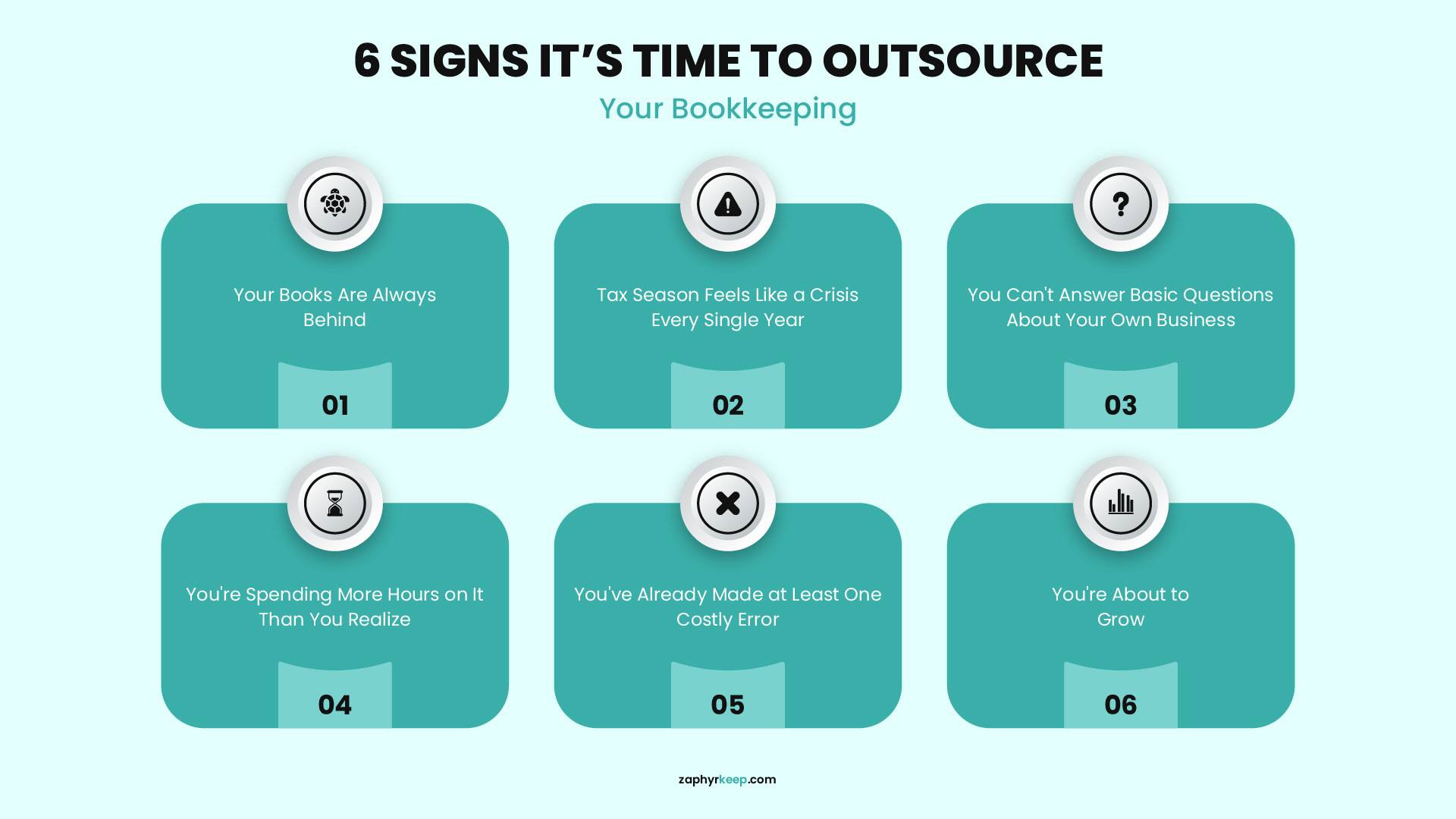

1. Your Books Are Always Behind

If you regularly work from records that are weeks or months out of date, every decision you make rests on information that no longer reflects reality. You might think cash flow looks fine when it doesn’t. You might miss that a major client hasn’t paid in 90 days.

You might overlook that your expenses crept up 20 percent last quarter without a single conscious decision driving that increase. Decisions made on stale financial data tend to be reactive rather than strategic, and reactive decisions almost always cost more in the long run.

2. Tax Season Feels Like a Crisis Every Single Year

If January and February bring that familiar sense of dread, a scramble to pull together a full year of transactions, and a messy pile handed to your accountant to sort out, the books clearly aren’t getting maintained throughout the year.

Your accountant charges you for that cleanup time at their full hourly rate. The IRS charges penalties if errors lead to late or incorrect filings. And you spend weeks stressed about something that proper bookkeeping maintenance would have made routine. That cycle repeats every single year until you change the system.

3. You Can't Answer Basic Questions About Your Own Business

Here’s a quick test. Without opening any software or digging through files, can you answer these right now? What’s your net profit this month? What do you currently owe vendors? How much estimated tax do you owe this quarter?

If the answer is no, your books aren’t doing their job, and that’s not a personal failing. It’s what happens when someone who didn’t train as a bookkeeper manages the records while simultaneously running an entire business. The solution isn’t to try harder. It’s to hand it to someone who does this as their full-time focus.

|

Factor

|

In-House Bookkeeping

|

Outsourced Bookkeeping

|

|---|---|---|

|

Cost

|

Salaries, benefits, training, and software costs add up

|

Pay for services as needed, often cheaper in the long run

|

|

Control

|

Direct oversight, instant access to financial data

|

Less control, but reports and updates are scheduled

|

|

Scalability

|

Hiring new staff is expensive and time-consuming

|

Scale services up or down based on business needs

|

|

Expertise

|

Limited to one person’s knowledge

|

Access to a team of specialists with industry expertise

|

|

Security

|

Data stays in-house, but security depends on internal protocols

|

Secure cloud-based systems with encryption and compliance measures

|

4. You're Spending More Hours on It Than You Realize

Most small business owners who honestly track the time they spend on bookkeeping find they log between five and fifteen hours a month on it, and sometimes significantly more during tax season or periods of high transaction volume.

According to a SCORE, small business owners often work excessively long hours (e.g., 39% over 60 hours/week per survey) and struggle with administrative overload, recommending delegation to free up time for growth activities.

Delegating financial tasks like bookkeeping is a widely recommended practice that helps owners focus more on revenue-generating work and avoid administrative backlogs, with the annual opportunity cost of those hours typically exceeding outsourcing fees.

5. You've Already Made at Least One Costly Error

Miscategorized expenses, a missed payroll tax deadline, a duplicate vendor payment, an invoice that never went out. These things happen when a non-specialist manages the books while running a full business at the same time.

The IRS charges a failure-to-deposit penalty of two to fifteen percent of unpaid payroll taxes depending on how late the deposit is. A single missed deadline can cost more than several months of professional bookkeeping. The risk isn’t hypothetical. It’s a regular reality for small business owners who stretch themselves too thin across too many roles.

6. You're About to Grow

More revenue means more transactions, and more transactions mean more complexity and more places for errors to hide. The bookkeeping process that worked at $300,000 a year will not hold up at $1 million.

Getting your books properly organized before a growth phase hits is significantly easier and cheaper than trying to clean them up after the volume has already increased. Growth creates momentum, and disorganized books slow that momentum down faster than most business owners expect until they’re already in the middle of it.

The Real Benefits of Outsourcing Bookkeeping

Once you’ve decided this might be the right move, it’s worth understanding what you actually gain in concrete terms.

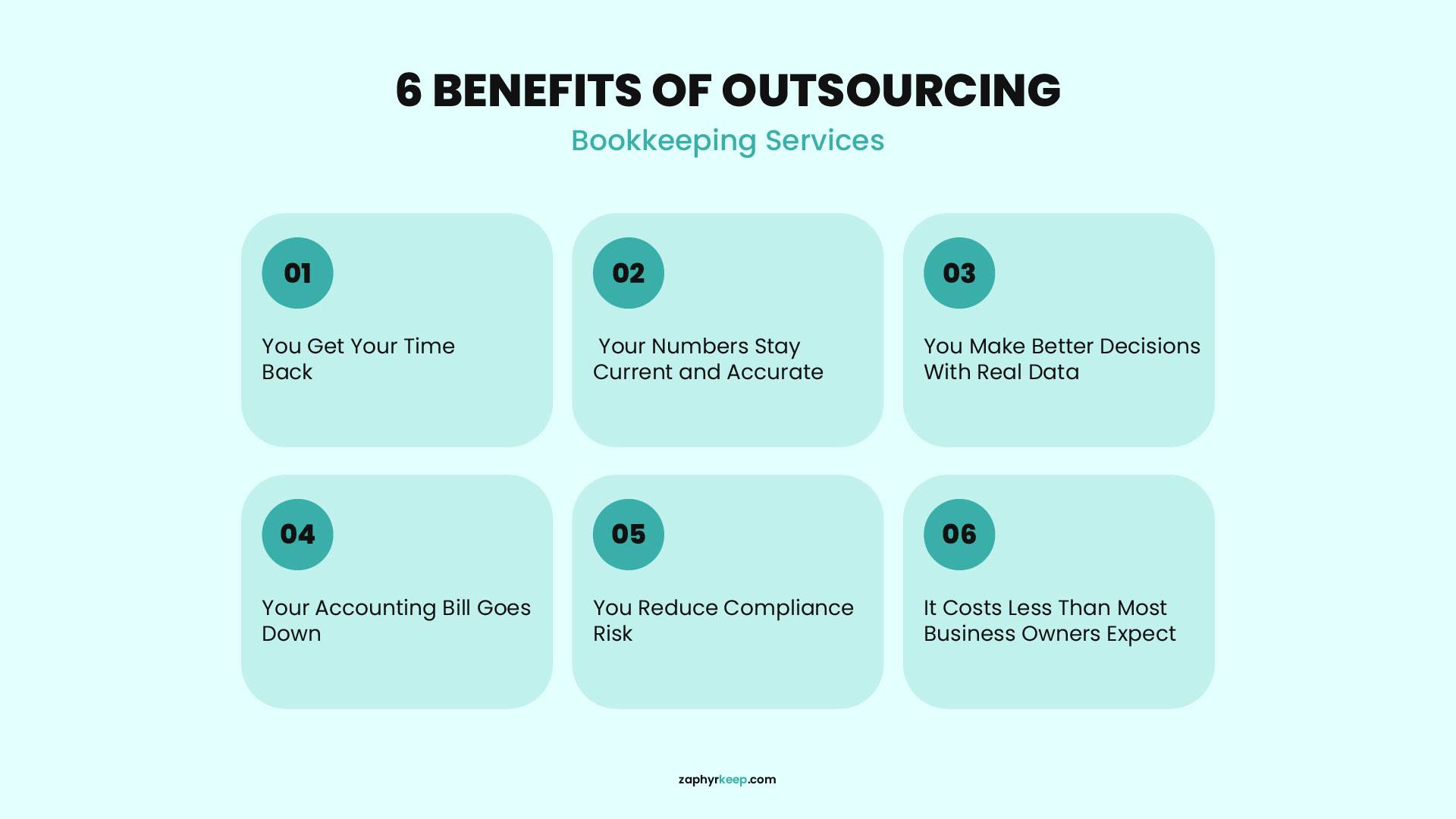

1. You Get Your Time Back

When you stop doing your own bookkeeping, you recover real hours every single month. Not just the time you spent doing the actual work, but the mental space you spent thinking about it, worrying about it, and postponing it.

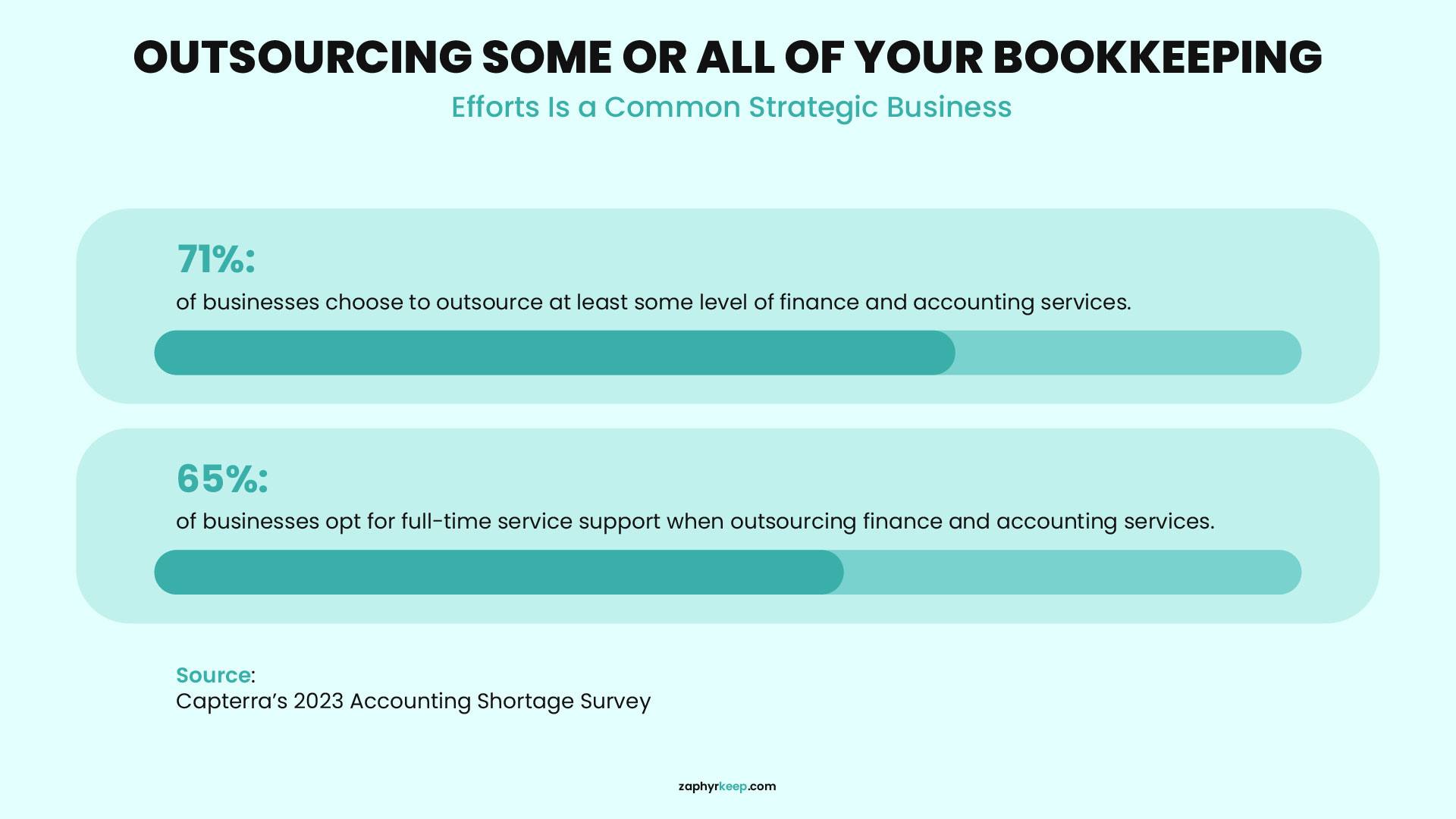

Clutch surveys of small businesses show that 27% outsource administrative and financial tasks primarily to save time and boost efficiency, freeing owners to focus on core growth areas like client work and revenue generation. That shift is harder to put a dollar figure on, but every business owner who makes it describes it as one of the best decisions they made.

2. Your Numbers Stay Current and Accurate

A professional bookkeeper works on a set schedule, not whenever a spare hour appears. Your books get updated regularly, which means every time you want to check your financial position, the numbers actually reflect what’s happening right now.

You stop making decisions based on data that’s two months old, and you start running your business with a real, current picture in front of you at all times. That accuracy compounds over time because clean records from month to month make every subsequent month faster and more reliable.

3. You Make Better Decisions With Real Data

This is the benefit most people underestimate before they experience it. When your books stay clean and current, you can see exactly where your money goes, which clients or product lines actually generate profit, where expenses quietly creep up, and whether your cash flow supports a new hire or a major purchase.

That level of financial clarity changes how you run the business. You stop operating on gut feel and start making calls backed by real numbers. Business owners who make that shift consistently report that it improves margins because they stop spending money on things that don’t earn their cost.

4. Your Accounting Bill Goes Down

Most accountants charge by the hour, and cleanup work takes a lot of hours. When your books arrive already clean, categorized, and reconciled, your accountant spends their time on tax strategy and planning rather than sorting through a year of disorganized transactions.

Well-maintained books can significantly reduce tax preparation time compared to disorganized ones, often by 30-50% based on common accounting estimates. At typical CPA rates of $200 to $400 per hour, that reduction adds up to real savings quickly, often enough to offset a significant portion of your monthly bookkeeping cost.

5. You Reduce Compliance Risk

Payroll taxes, sales tax filings, and quarterly estimated payments all carry firm deadlines and automatic penalties. The IRS failure-to-deposit penalty starts at two percent for deposits one to five days late and climbs to fifteen percent if the agency issues a formal notice before you act.

A good bookkeeper tracks your obligations and makes sure you meet every deadline. You stop relying on memory or a calendar reminder to catch things that carry real financial consequences, and you stop discovering compliance problems after they’ve already turned into expensive ones.

6. It Costs Less Than Most Business Owners Expect

A full-time bookkeeper in the US typically costs employers $40,000–$55,000 annually in base salary (national average around $45,000), before adding benefits, payroll taxes (adding ~10%), and absence coverage.

Outsourcing typically runs between $300 and $2,000 per month depending on transaction volume and what’s included. For most small businesses doing under $5 million a year in revenue, the cost comparison isn’t close. You get professional-level work at a fraction of the total cost, without the management overhead that comes with a direct hire.

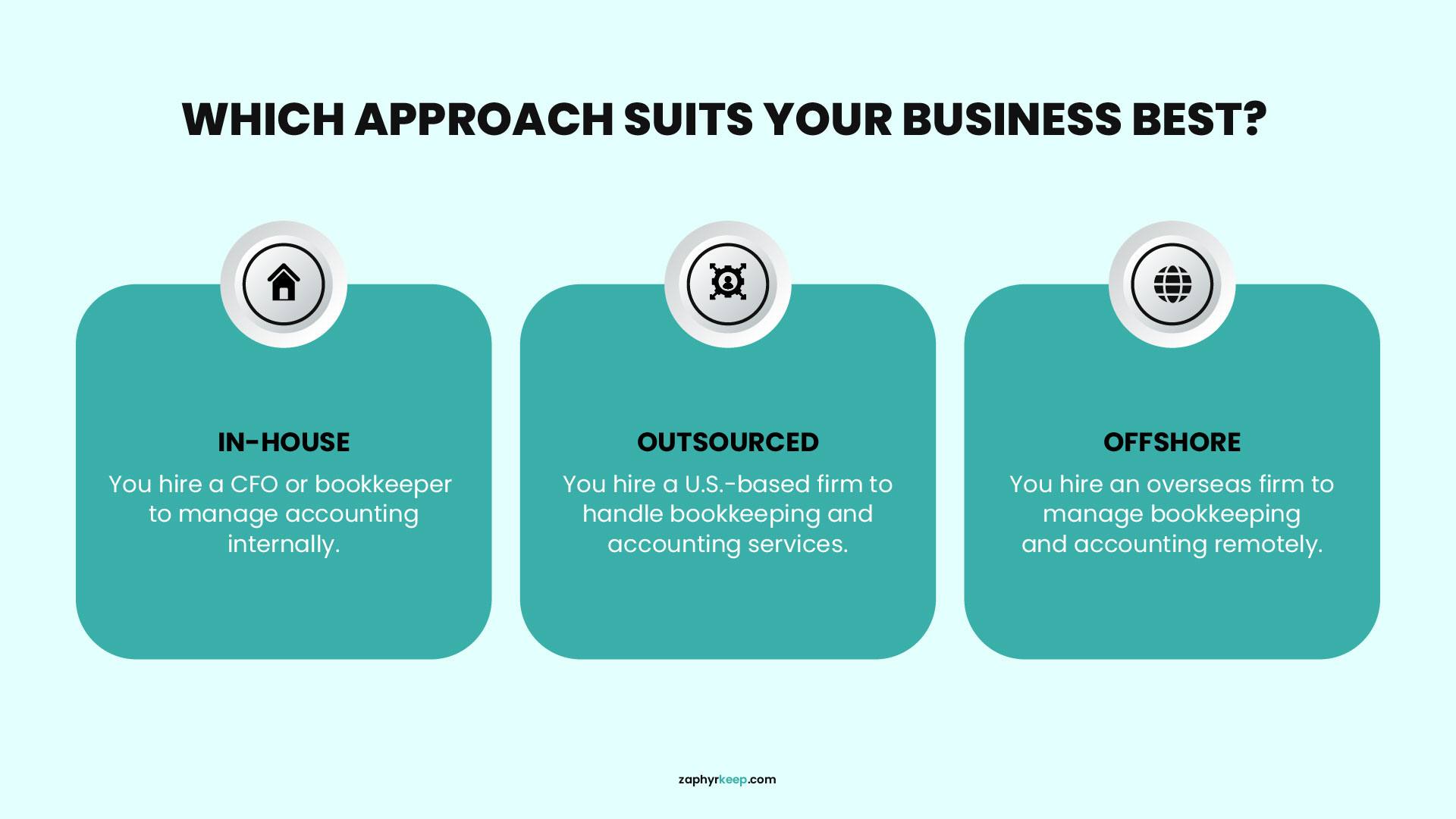

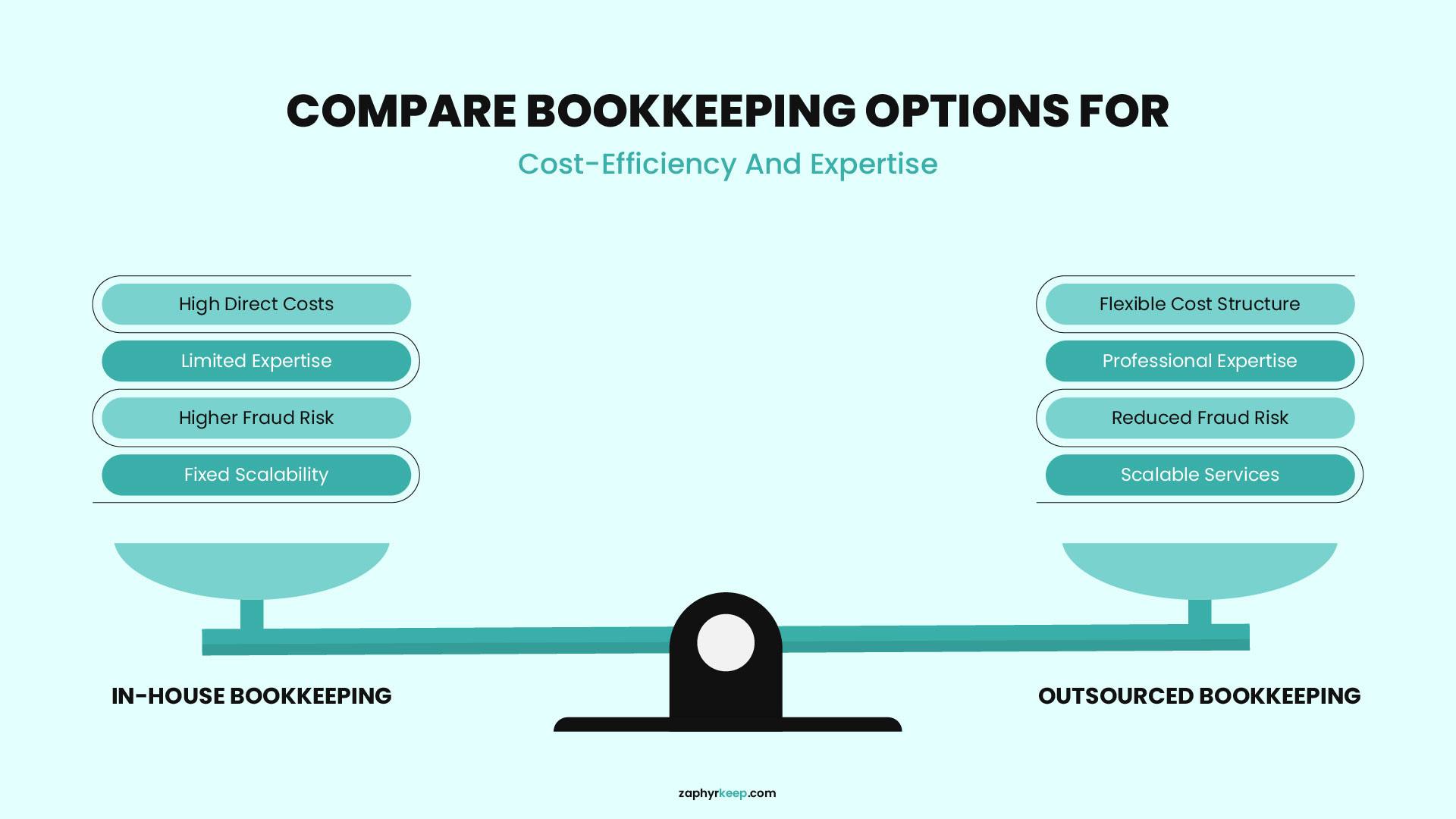

Outsourced Bookkeeping vs. Keeping It In House

Both options work. The right one depends on your business. So instead of just saying outsourcing is always better, here’s an honest look at both.

When In House Makes Sense

If your transaction volume genuinely requires daily attention inside your books, a full-time hire starts to make financial sense. The same applies if your operations are complex enough that you need someone deeply embedded in your business processes, not just someone processing records from the outside.

Some businesses, particularly cash-heavy retail operations or businesses with complicated inventory management, benefit from having someone physically available throughout the day who knows the operation intimately and can respond to issues as they come up.

When Outsourcing Makes More Sense

For most small and medium businesses doing under $5 million a year, outsourcing delivers better value financially and operationally. You get professional work at a fraction of the cost of a full-time hire, and you don’t depend on a single person, so if your bookkeeper gets sick or moves on, the work continues without interruption.

You also gain access to a team that has worked across many different types of businesses and industries, which means fewer rookie mistakes around industry-specific accounting nuances. And you avoid the time and energy cost of hiring, training, managing, and eventually replacing an employee.

What’s The Hybrid Approach?

Many businesses start with outsourcing and bring someone in house later as they scale and the volume genuinely justifies a full-time role. That’s a completely reasonable path, and it’s more common than most people realize. Outsourcing gives you a stable, professional foundation while the business grows, and you can reassess whenever the numbers and the workload say it’s time. You don’t need to commit to one approach permanently right now.

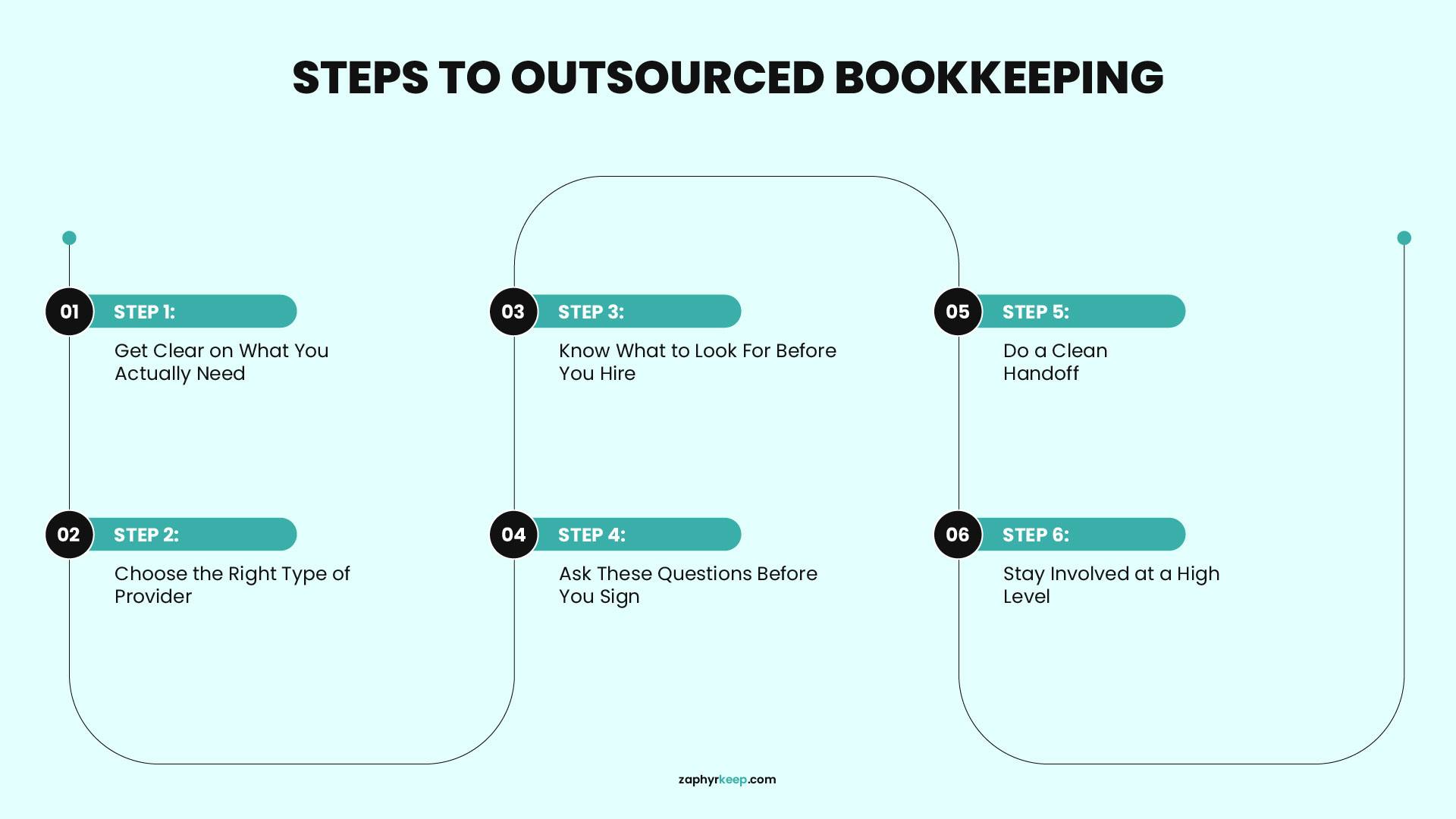

How to Outsource Your Bookkeeping: Step by Step

Knowing you need to outsource is one thing. Doing it well enough to avoid the common frustrations is another. Here’s how to approach the process the right way.

Step 1: Get Clear on What ou Actually Need

Before you talk to any provider, write down exactly what you want to hand off. Basic transaction categorization? Bank reconciliations? Accounts payable and receivable management? Payroll processing? Monthly financial reports?

The more specific you are going in, the easier it becomes to find the right match, get an accurate quote, and avoid the scope misunderstandings that create friction three months in. Vague handoffs lead to gaps, and gaps in bookkeeping compound quickly into problems that cost real money to fix.

Step 2: Choose the Right Type of Provider

There are a few types of outsourced bookkeeping, and they’re not all the same.

- A freelance bookkeeper works independently. Usually the lowest cost option. Good for straightforward books at lower transaction volumes. The risk is that if they’re unavailable, your books stop moving.

- A bookkeeping firm gives you access to a team. More reliable, more consistent, and usually better equipped to handle growth or complexity. Typically costs more than a solo freelancer but less than an in house hire.

- An offshore bookkeeping provider can cut costs significantly, sometimes by 50 percent or more compared to US based options. Quality varies widely so due diligence matters more here. Look for providers with strong reviews, clear communication, and experience with US accounting standards.

Step 3: Know What to Look For Before You Hire

These are the factors that actually separate a reliable provider from one that quietly creates more problems than they solve.

- Responsiveness matters more than most people realize going in. You should not have to wait two days to get a basic answer about your own finances. Before you hire anyone, find out how they communicate, what their typical response time is, and who your direct point of contact will be day to day.

- Industry experience directly affects the quality of the work. A bookkeeper who works primarily with e-commerce businesses understands inventory accounting, merchant fee categorization, and platform-specific revenue tracking in a way that a generalist might not. Ask whether they have experience with businesses in your industry before you commit.

- The tools they use determine how much visibility you actually have into your own records. Any provider worth hiring uses modern, cloud-based software that gives you shared, real-time access to your books. If you can’t log in and see your own finances at any time, that arrangement doesn’t work in your favor.

- Their process for handling errors tells you a lot about their character. Ask directly: what happens when you make a mistake? A trustworthy provider gives you a clear, straightforward answer. They own the error, fix it, and communicate it to you. Vague or defensive answers to this question are a genuine warning sign.

- Who actually touches your books is a question many people forget to ask. Some firms pitch you with senior staff during the sales conversation and then hand your account to a junior team member. Know exactly who will work on your books before you sign anything.

Step 4: Ask These Questions Before You Sign

A 20-minute conversation before you hire saves significant frustration later. Ask every provider: How many clients do you currently manage? What’s your average turnaround time for monthly close? How do you handle catch-up bookkeeping if my records are behind? What accounting software do you use and will I have full access at all times? How do you protect client financial data? What’s included in my monthly fee and what triggers an additional charge?

Their willingness to answer clearly and specifically tells you as much as the answers themselves. A provider who gets vague or defensive during a pre-hire conversation will be harder to work with once you’ve already signed.

Step 5: Do a Clean Handoff

Once you hire someone, invest real time in proper onboarding. Give them access to your accounting software, bank accounts, and credit card feeds, and then walk them through your business model, your main revenue streams, your regular expense categories, and any recurring transactions or unusual arrangements they need to know about.

The more context you provide upfront, the less back and forth you deal with during the first few months, and the fewer errors show up in the early reports. A rushed or incomplete handoff is one of the most common reasons outsourced bookkeeping starts poorly even when the provider is genuinely competent.

Step 6: Stay Involved at a High Level

Outsourcing your bookkeeping doesn’t mean you stop paying attention to your own finances. Every month, review your profit and loss statement, your cash flow summary, your outstanding invoices, and what you currently owe. You don’t need to reconcile accounts or categorize transactions yourself.

But you do need to understand the financial headlines of your own business because staying engaged at this level means you catch developing problems early rather than discovering them at tax time when your options for addressing them are much more limited.

What Does It Cost to Outsource Bookkeeping?

Pricing depends on your transaction volume, the complexity of your books, and the type of provider you choose. Here’s a realistic breakdown of what to expect in 2026.

- Freelance bookkeeper: Roughly $25 to $60 per hour, or $200 to $800 per month for basic ongoing services. The lower end of this range covers simple categorization and reconciliation for a business with low transaction volume and a single bank account.

- US-based bookkeeping firm: Typically $500 to $2,500 per month depending on scope and monthly transaction count. Firms at the higher end usually include payroll processing, accounts payable and receivable management, and detailed monthly financial reporting.

- Offshore bookkeeping provider: Usually $150 to $800 per month for work comparable to a mid-range US-based service. The cost savings are real, but so is the variation in quality. Vet offshore providers more carefully than you would a domestic firm.

- Catch-up bookkeeping: If your records are behind, most providers charge separately for cleanup before they move you onto a regular monthly plan. Expect to pay around $150 to $400 per month of backlog, and sometimes more if the records span multiple years or are particularly disorganized.

Most providers offer a free consultation and a custom quote once they understand your situation. The advice worth repeating here: don’t make the final decision on price alone.

A bookkeeper who misses transactions, goes quiet when you ask questions, or makes recurring errors will cost you far more in accountant cleanup fees and compliance penalties than you ever saved on the monthly rate.

Common Mistakes to Avoid

Most of the problems people run into with outsourced bookkeeping trace back to a handful of avoidable errors. Knowing them in advance means you don’t have to learn them the hard way.

Waiting Too Long to Start

The longer you delay, the more the books pile up and the more expensive the cleanup becomes. Catch-up bookkeeping for a business that’s six months behind costs significantly more than simply starting on time. If you already know you need help, the right time to act is now, not after tax season, not after you close the next big client, and not after the backlog gets worse.

Choosing on Price Alone

A $200-per-month bookkeeper sounds like a deal until you discover they’re managing 60 clients and giving your account a few hours of attention each month. Low price and low quality tend to travel together in this industry. Ask specifically what’s included in the quoted price, how many hours they plan to spend on your account monthly, and what happens when the volume increases before you commit to anything.

Handing It Off and Completely Disconnecting

Your bookkeeper manages the records, but you still need to understand your own financials. Business owners who stop looking at their numbers entirely tend to miss slow-building problems, like a cash flow gap that develops over several months, until it becomes a crisis. A monthly 15-minute review of your key reports keeps you informed without pulling you back into the weeds.

Skipping the Written Agreement

Before anyone touches your books, put a clear written agreement in place. That agreement should cover the scope of work, turnaround times, how they protect your financial data, what happens to your records if you end the relationship, and how disputes get resolved. Verbal agreements feel fine at the start and create real problems later.

Not Verifying Credentials

Ask whether they hold relevant certifications like a Certified Bookkeeper designation or a QuickBooks ProAdvisor certification. Neither is a guarantee of quality on its own, but both signal that the person takes the work seriously and has met a recognized standard of knowledge. An uncredentialed provider isn’t automatically a bad choice, but it’s a reason to ask more questions and check references more carefully.

Skipping a Trial Period

Before you commit to a long-term arrangement, ask if you can start with one or two months to see how the relationship actually works in practice. Most good providers welcome this because they’re confident in their work. If a provider pushes back hard on a trial period, pay attention to that reaction. It tells you something about how they operate when a client wants accountability.

Ready to Stop Doing Your Own Books?

Outsourcing your bookkeeping makes sense when your time is better spent elsewhere, when your books are behind or inaccurate, when you’re growing, or when you’re spending real hours every month on something you didn’t start your business to do.

It’s not complicated to set up. It’s more affordable than most people expect. And the businesses that do it well end up with cleaner numbers, lower accounting bills, and a much clearer picture of how the business is actually performing.

The books still have to get done. The only real question is whether you’re the right person to be doing them.

If you’re ready to hand it off, we can help. Get a free quote today and find out exactly what outsourced bookkeeping services would look like for your business.

Frequently Asked Questions

What is outsourced bookkeeping for small businesses?

+Outsourced bookkeeping means hiring an outside person or company to manage your financial records instead of handling them yourself or keeping a bookkeeper on your payroll. The provider tracks your income and expenses, reconciles your bank accounts, manages payroll records, and delivers clean monthly financial reports. You keep full visibility into your books at all times, but the day-to-day work of maintaining them moves off your plate entirely.

What are the main benefits of outsourcing bookkeeping?

+The biggest benefits are time savings, financial accuracy, and lower overall costs. You stop spending hours on tasks outside your core skills and start working from current, accurate numbers every month. Clean books also reduce what you pay your accountant at tax time, since they spend less time on cleanup and more on strategy. On top of that, a professional bookkeeper tracks your compliance deadlines and keeps you out of IRS penalty territory.

How much does it cost to outsource bookkeeping for a small business?

+Costs vary based on transaction volume and the type of provider you choose. A freelance bookkeeper typically charges $200 to $800 per month for basic services. A US-based bookkeeping firm usually runs $500 to $2,500 per month. Offshore providers generally fall between $150 and $800 per month. If your records are behind, most providers charge an additional one-time catch-up fee of $150 to $400 per month of backlog before starting regular monthly service.

How do I outsource bookkeeping for my small business?

+Start by listing exactly what you need: transaction categorization, bank reconciliations, payroll, reporting, or some combination. Then choose between a freelance bookkeeper, a bookkeeping firm, or an offshore provider based on your budget and volume. Before signing anything, ask about their response times, software, credentials, and what happens if they make an error. Once you hire, do a thorough onboarding so they understand your business, and review your financial reports every month to stay informed.

Is outsourcing bookkeeping worth it for small businesses?

+For most small businesses, yes. The cost of outsourcing typically runs well below the cost of hiring a full-time bookkeeper, which averages around $45,000 per year in salary alone according to the Bureau of Labor Statistics, before benefits and overhead. Beyond the direct cost savings, clean and current books lead to better business decisions, lower accounting fees, and fewer compliance penalties. Business owners who outsource consistently report that the time and mental energy they recover is worth as much as the financial savings.